The Carbon Border Adjustment Mechanism (CBAM)

14 min

Level

In this article, we break down what the EU CBAM is, how it works, and what businesses need to do to comply.

ESG / CSR

Industries

By Kara Anderson, UK Copywriter, on 13/02/2025

Updated by Kara Anderson, on 27/05/2026

The Corporate Sustainability Reporting Directive (CSRD) has fundamentally transformed how businesses approach sustainability. At the heart of this shift is the Impacts, Risks, and Opportunities (IRO) framework - a mandate that requires companies to look both outward at their societal footprint and inward at their financial resilience.

IROs act as the filter for your entire sustainability report. By systematically mapping out where your business impacts the world and where sustainability trends create commercial risks and opportunities, you can cut through the noise. This framework ensures your business prioritises and discloses exactly what matters under the European Sustainability Reporting Standards (ESRS).

What are IROs?

The Role of Double Materiality

Step-by-Step Identification & Assessment

CSRD Disclosure Requirements (IRO-1 & IRO-2)

Challenges & Best Practices

The Impacts, Risks, and Opportunities (IROs) framework is the operational backbone of sustainability reporting under the Corporate Sustainability Reporting Directive (CSRD). Rather than treating sustainability as a vague corporate social responsibility exercise, the IRO framework forces companies to categorise and quantify how sustainability issues affect both the wider world and their own financial bottom line.

Under the European Sustainability Reporting Standards (ESRS), these three distinct lenses are defined as:

Under CSRD, companies cannot simply pick and choose what they want to report. They must pass all potential sustainability topics through a rigorous double materiality assessment to determine what is truly significant to their business.

Ultimately, IROs dictate the boundaries of your entire CSRD report. By systematically analysing where your company has an impact, where it faces financial risk, and where it can capture green opportunities, you establish a clear, auditor-ready roadmap. This roadmap determines exactly which ESRS topical disclosures are mandatory for your business and how your final reporting must be structured.

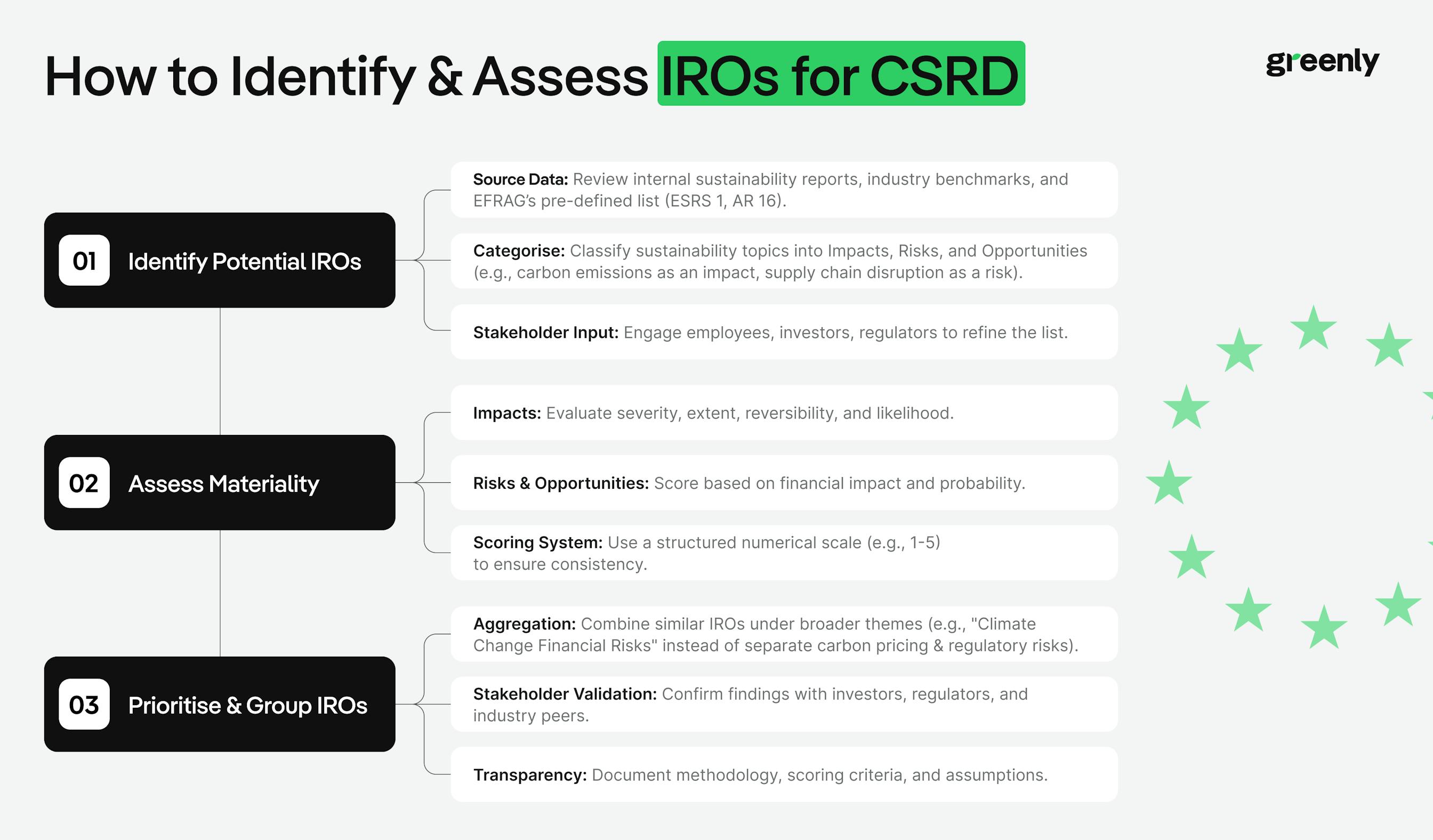

Identifying your Impacts, Risks, and Opportunities (IROs) is the critical baseline of CSRD reporting. Without a structured identification phase, companies risk missing critical vulnerabilities or wasting resources tracking immaterial data.

According to EFRAG's Materiality Assessment Implementation Guidance (IG 1), this mapping process should be broken down into three distinct operational steps:

Companies should avoid guessing what might be material. Instead, they should anchor the process in ESRS 1, Appendix A, AR 16, which provides a predefined taxonomy of sustainability topics, sub-topics, and sub-sub-topics.

This list should then be complemented by internal data, such as risk registers or HR metrics, peer benchmarks, and early-stage stakeholder engagement with investors, employees, and suppliers to catch blind spots before data modelling begins.

Once your longlist is established, separate the issues into explicit categories. A single sustainability topic will often generate multiple distinct items across the IRO framework.

A company’s sustainability footprint rarely stops at its factory doors or office walls. Under the CSRD, IROs must be mapped across three distinct horizons.

Once your Impacts, Risks, and Opportunities are mapped, you must evaluate which ones cross the threshold into being material. Under the CSRD’s double materiality mandate, this evaluation requires two distinct scoring lenses: Severity & Likelihood for impacts, and Financial Performance & Probability for risks and opportunities.

For impacts, materiality is determined by severity. Under ESRS 1, severity is assessed using three core criteria - scale, extent, and reversibility - with likelihood added only for potential future impacts.

Unlike the inside-out perspective used for impacts, financial materiality focuses on how sustainability topics influence value creation, cash flow, asset preservation, and long-term business resilience.

Measures the estimated economic effect of a risk or opportunity, including liabilities such as regulatory fines and carbon taxes, or gains such as efficiency savings and green market growth.

Evaluates the likelihood that a financial risk or opportunity will materialise over a defined reporting horizon.

After scoring your list, the final phase involves refining your data so it is clear, structured, and auditable.

A robust identification process can produce hundreds of granular findings. Rather than listing every issue individually, companies should consolidate related findings into broader sustainability themes, following EFRAG’s Materiality Assessment Guidance.

Although stakeholder engagement is not strictly mandatory under the ESRS, EFRAG strongly recommends it as a validation mechanism to strengthen the credibility and completeness of the assessment.

The final test of a materiality assessment is whether it is transparent and auditable. Every included or excluded IRO should be supported by a clearly documented methodology.

By maintaining this transparent trail, your business ensures a seamless path to compliance, giving assurance providers the exact verification details they require.

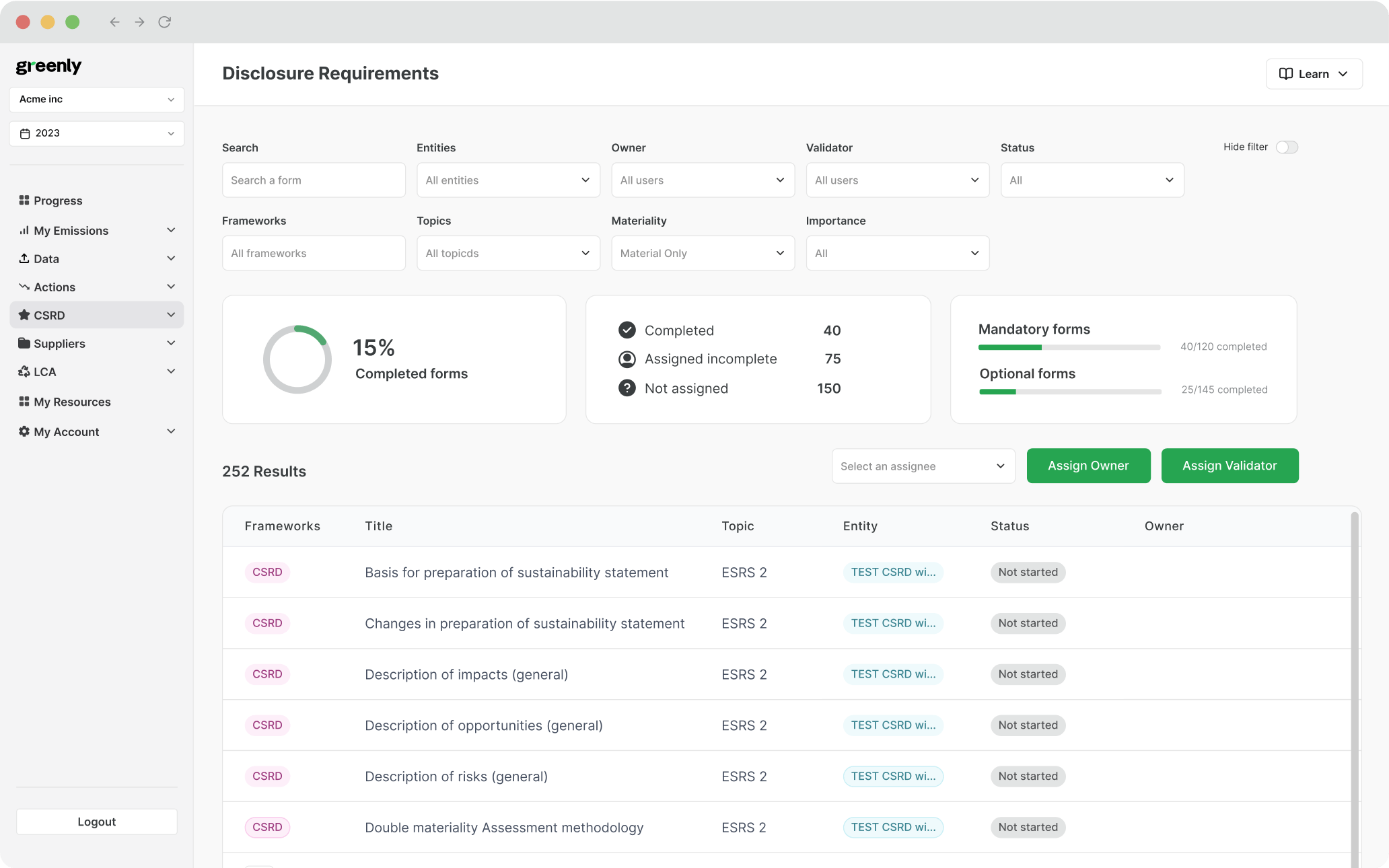

Once your Impacts, Risks, and Opportunities (IROs) have been identified and scored, they must be formally translated into your sustainability statement. Under ESRS 2 (General Disclosures), companies cannot simply publish a random list of green initiatives. You must follow a strict, structured disclosure blueprint governed by three core requirements:

Together, these disclosures provide investors, regulators, and assurance providers with a transparent view of your compliance methodology.

ESRS E1 on climate change carries a particularly high bar for exclusion. If a company concludes that climate change is not material, it cannot simply omit the section.

Under ESRS 2 IRO-2, the company must provide a detailed, data-backed explanation, including forward-looking analysis showing which future operational or environmental conditions would need to hold true for climate change to remain non-material.

Because this justification is heavily scrutinised by external auditors, most European undertakings treat ESRS E1 as a baseline disclosure.

setting up a great IRO process looks good on paper, but executing it in the real world is tough. It requires mixing environmental data with financial forecasting - two departments that historically haven't spent a lot of time talking to each other.

If you are running into roadblocks, you aren't alone. Here are the five biggest challenges companies face right now, along with practical ways to solve them.

Mapping IROs across the value chain requires data from suppliers, HR systems, factory operations, and finance teams. Tracking areas like Scope 3 emissions or supplier working conditions can quickly become fragmented and unreliable.

Start small and build a structured data diary. Document gaps, use reliable industry averages where necessary, and centralise information into a dedicated sustainability platform instead of relying on disconnected spreadsheets.

Investors may focus primarily on financial risk, while employees and communities prioritize environmental and social impacts. Balancing competing expectations makes it difficult to determine what is truly material.

Run structured stakeholder workshops with internal and external groups. Present findings clearly, facilitate discussion, and document the rationale behind the final priorities selected.

The ESRS framework explains what should be assessed, but it does not provide a universal scoring formula. Teams may disagree over whether a risk qualifies as moderate or severe.

Build a shared glossary before scoring begins. Define what terms like “high impact” or “severe risk” mean in operational or financial terms to ensure consistency across departments.

Companies already reporting under frameworks like GRI, SASB, or TCFD often feel they are duplicating the same work again under CSRD requirements.

Use EFRAG interoperability guidance to build one centralised reporting structure. By mapping once against core CSRD requirements, companies can often satisfy multiple frameworks simultaneously.

Climate events, regulations, and consumer expectations evolve rapidly, meaning a materiality assessment completed a year ago can quickly become outdated.

Treat your IRO register as a living document. Integrate reviews into quarterly risk meetings and reassess material topics whenever major operational or strategic changes occur.

Simply put, it’s about direction. An impact is an inside-out view - it’s how your company’s actions affect the outside world (like your factory polluting a local river). A risk is an outside-in view - it’s how the outside world threatens your company’s financial health (like a new environmental law forcing you to buy expensive clean-up equipment). Under CSRD, you have to report on both.

No. During your assessment, you will likely find dozens or even hundreds of potential IROs. You are only required to disclose the ones that pass your internal materiality threshold - meaning they have a significant impact on the planet or a meaningful financial effect on your business. You must, however, document why you excluded the minor ones so you can show your auditors.

Under the CSRD, the company’s board of directors or administrative management body must formally review and sign off on the double materiality assessment and the finalised list of material IROs. It cannot just be approved by the sustainability team; leadership must demonstrate active oversight.

You must review and update your IRO assessment annually as part of your regular management report. However, if your business undergoes a major change mid-year - such as a massive merger, entering a completely new geographic market, or a drastic shift in supply chain regulations - you should update your IRO registry dynamically to reflect those new realities.

This is a major red flag for external auditors. Your financial risk register and your CSRD sustainability disclosures must be fully aligned. If your IRO assessment claims that climate change poses a severe risk to your operations, but your corporate risk register doesn't mention it, auditors will challenge your methodology. This is why cross-functional teamwork between finance and sustainability is so important.

While listed SMEs do fall under the scope of CSRD, they use a simplified set of standards known as LSME (Listed SMEs). The core concept of identifying Impacts, Risks, and Opportunities still applies, but the scoring expectations, value chain reporting boundaries, and data points are much less demanding than those for large multinational corporations.

Share this article

In this article, we break down what the EU CBAM is, how it works, and what businesses need to do to comply.

What is decarbonisation and why is it urgent? Learn practical steps companies can take to support the global move toward net zero emissions.