Decarbonisation: what it is and why it matters

1 min

Level

What is decarbonisation and why is it urgent? Learn practical steps companies can take to support the global move toward net zero emissions.

ESG / CSR

Industries

By Stephanie Safdie, US Copywriter, on 29/09/2022

Updated by Stephanie Safdie, on 20/01/2026

For companies today, transparency is central to building trust with employees, customers, investors, and local communities. From health and safety and waste management to energy use, social impacts, and community engagement, sustainability issues now cut across almost every part of a business. In many cases, they’re also tied to growing regulatory and reporting expectations.

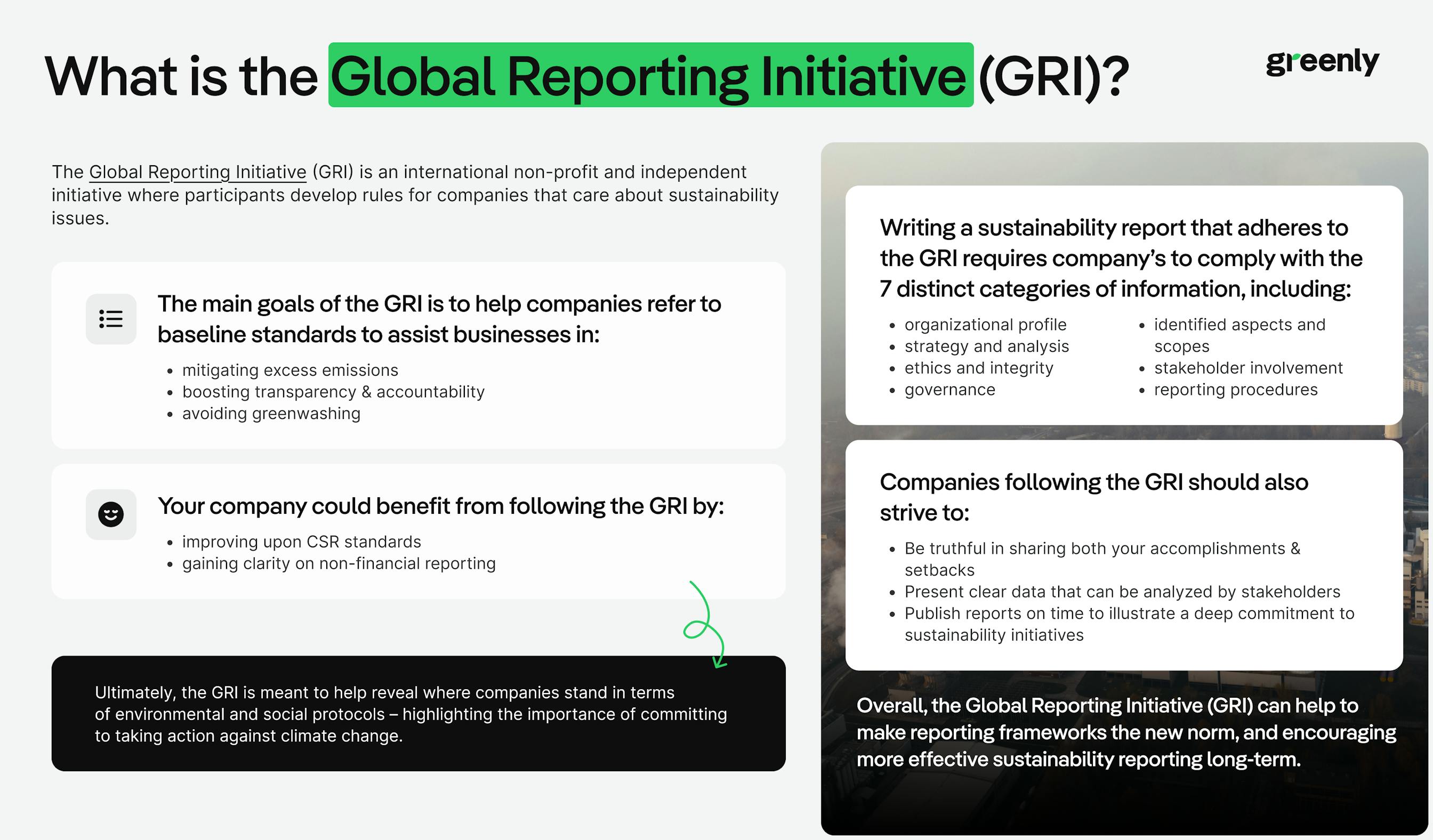

But communicating these impacts clearly and credibly isn’t always straightforward. To do it well, companies need consistent indicators, shared definitions, and a recognised structure for reporting their performance. This is where the Global Reporting Initiative (GRI) comes in.

The GRI provides an internationally recognised framework for sustainability reporting, helping organisations measure and disclose their environmental, social, and economic impacts in a structured and comparable way. While the GRI Standards are not legally mandatory, they are widely used by companies worldwide as a trusted reference for transparent and credible sustainability reporting.

What the Global Reporting Initiative (GRI) is and how it’s used

The core principles and reporting requirements behind the GRI Standards

The main goals and business benefits of GRI reporting

How companies can implement GRI step by step

The Global Reporting Initiative (GRI) is an independent, international non-profit organisation that develops widely used standards for sustainability reporting. Its goal is to help companies understand, measure, and communicate their environmental, social, and economic impacts in a clear and consistent way.

There is no official “GRI certification” or label - it's a completely voluntary reporting framework. Instead, companies choose to apply the GRI Standard. This means that the GRI framework is particularly well-suited to organisations that want to:

Rather than being written in isolation, the GRI Standards are developed with input from a wide range of organisations and experts, including:

This mix of contributors helps keep the GRI Standards grounded in real-world sustainability challenges. In practice, the guidelines give companies a shared framework for reporting their economic, social, and environmental impacts in a way that is both transparent and comparable.

Reporting under the Global Reporting Initiative (GRI) framework is voluntary, but it follows a clearly defined structure. Companies that choose to use the GRI Standards are expected to apply a consistent methodology, focus on what truly matters, and provide transparent, comparable sustainability information to stakeholders.

Rather than prescribing a single reporting format, GRI sets out a series of core requirements that guide how organisations identify, measure, and disclose their environmental, social, and economic impacts.

The goal of GRI reporting is simple: to make a company’s environmental and social performance visible and comparable. It gives organisations a clear way to show where they stand, based on evidence rather than claims.

By setting common indicators and disclosure requirements, the GRI framework helps companies assess whether their sustainability actions are delivering real results and track progress over time.

More broadly, this kind of reporting supports better decisions - inside and outside the organisation. It strengthens governance and risk management, enables stakeholder scrutiny, and provides a foundation for continuous improvement and meaningful climate action.

The Global Reporting Initiative (GRI) was founded in 1997 in the United States, emerging from a collaboration between CERES (the Coalition for Environmentally Responsible Economies) and the United Nations Environment Programme (UNEP). The aim was clear from the start: to create a common language for organisations to report on sustainability impacts.

Over time, GRI evolved from a set of early guidelines into the globally recognised reporting framework used today. Oversight of the standards now sits with the Global Sustainability Standards Board (GSSB), which is responsible for reviewing existing standards and developing new ones to reflect emerging sustainability challenges.

2000 – The first GRI sustainability reporting guidelines are released. For the first time, organisations are given a shared framework to report on environmental, social, and economic impacts.

2002 & 2006 – The guidelines are revised. Indicators and disclosures are note refined to improve clarity, consistency, and usability across sectors.

2013 – GRI G4 is introduced. The framework is significantly updated, placing stronger emphasis on materiality and impact-focused reporting.

2016 – GRI transitions to the GRI Standards. The guidelines evolve into a modular standards-based structure and align more closely with the UN Sustainable Development Goals (SDGs).

Today – The GRI Standards continue to evolve. Universal, topic, and sector standards reflect the most significant economic, environmental, and social impacts across industries.

The GRI Standards help companies clearly explain their sustainability impacts. They provide a practical structure for measuring what matters and tracking progress over time.

For stakeholders, GRI reporting makes sustainability information easier to understand and compare, helping build trust in what companies report.

Implementing the GRI Standards isn’t about ticking boxes or selecting a few indicators at random. It’s about putting a clear structure around how your organisation understands, measures, and communicates its impacts.

Here’s how companies typically approach it in practice:

GRI reporting works best when it’s owned internally, rather than treated as a one-off reporting exercise. Most organisations start by appointing a small, cross-functional team responsible for sustainability and non-financial reporting.

That team doesn’t need to be made up of specialists from day one, but they do need a shared understanding of sustainability issues and how the GRI framework works. Training teams on GRI principles helps ensure everyone understands:

When employees understand the “why” behind the data, engagement is much stronger, and reporting becomes more than a compliance task.

GRI reporting follows a defined methodology, guided by two sets of principles: content principles and quality principles. Together, they shape what goes into the report and how information is presented.

Content principles help determine what should be reported. They encourage companies to:

Quality principles, on the other hand, focus on how information is reported. They are designed to ensure disclosures are:

Following these principles helps ensure reports are credible and useful - not just well-intentioned.

Once the organisation has identified its material topics, the next step is selecting the GRI Standards that apply. This usually includes:

From there, companies define the indicators and data points needed to report consistently on each topic.

To bring everything together, organisations complete a GRI content index (sometimes called a GRI reference table). This acts as a roadmap for readers, showing exactly where each required disclosure can be found.

The index typically includes:

This step ensures the report is structured, transparent, and easy to navigate.

Finally, GRI reporting isn’t meant to be static. Companies are encouraged to use insights from their reports to track progress over time, improve decision-making, and refine sustainability strategies year after year.

It’s no coincidence that a large majority of the world’s biggest companies use GRI Standards as a foundation for their sustainability reporting - the framework provides a shared language that works across sectors, regions, and audiences.

No. Reporting under the Global Reporting Initiative (GRI) Standards is voluntary. There is no legal obligation to publish a GRI-compliant report, and there is no official “GRI certification”. That said, many companies use GRI because it is widely recognised by investors, customers, and regulators as a credible way to structure sustainability disclosures - especially where transparency and comparability matter.

Yes. GRI is commonly used alongside other frameworks rather than on its own. Many companies rely on GRI for impact-based sustainability reporting while also using frameworks such as ESRS for CSRD compliance in the EU or ISSB standards for investor-focused disclosures. GRI focuses on how a company impacts the economy, environment, and society, which complements financial risk–based reporting rather than duplicating it.

No, but the concepts are closely linked. CSR refers to a company’s overall approach to social and environmental responsibility, while ESG is often used by investors to assess performance and risk. GRI is a reporting framework that helps companies disclose sustainability impacts in a structured and consistent way. It does not define a CSR strategy, but it helps explain and evidence it.

GRI does not provide labels or certifications, but it can support them indirectly. Many sustainability ratings and assessments, such as EcoVadis, draw on international standards, including GR,I when evaluating company practices. Using GRI indicators can make it easier to organise data, demonstrate transparency, and respond to assessment questionnaires without duplicating effort.

No. GRI G4 was an earlier version of the framework and is now outdated. Today, companies use the GRI Standards, which are modular and regularly updated. These include Universal Standards, Topic Standards, and Sector Standards designed to reflect the most significant impacts across industries.

A GRI-aligned report usually explains the organisation’s activities, identifies its material sustainability topics, presents disclosures linked to relevant GRI Standards, and includes a GRI content index showing where information can be found. The level of detail varies, but clarity, consistency, and transparency are central.

Yes. Because GRI reporting is based on defined disclosures, indicators, and reporting principles, it encourages companies to support sustainability claims with data. This makes reporting more credible and helps stakeholders distinguish between genuine action and vague or unsupported claims.

In the UK, companies face a mix of mandatory and voluntary sustainability reporting requirements, including SECR, TCFD-aligned climate disclosures, and emerging UK Sustainability Disclosure Standards (SDS). While GRI is not required under UK law, many organisations use it alongside these frameworks to structure their environmental and social disclosures. GRI helps provide consistency and transparency across reports, making it easier to meet stakeholder expectations and align UK reporting with international best practice.

Share this article

What is decarbonisation and why is it urgent? Learn practical steps companies can take to support the global move toward net zero emissions.

In this article, we’ll break down what IROs are, how to identify and assess them, and what CSRD requires in terms of disclosure.

In this article, we break down what the EU CBAM is, how it works, and what businesses need to do to comply.