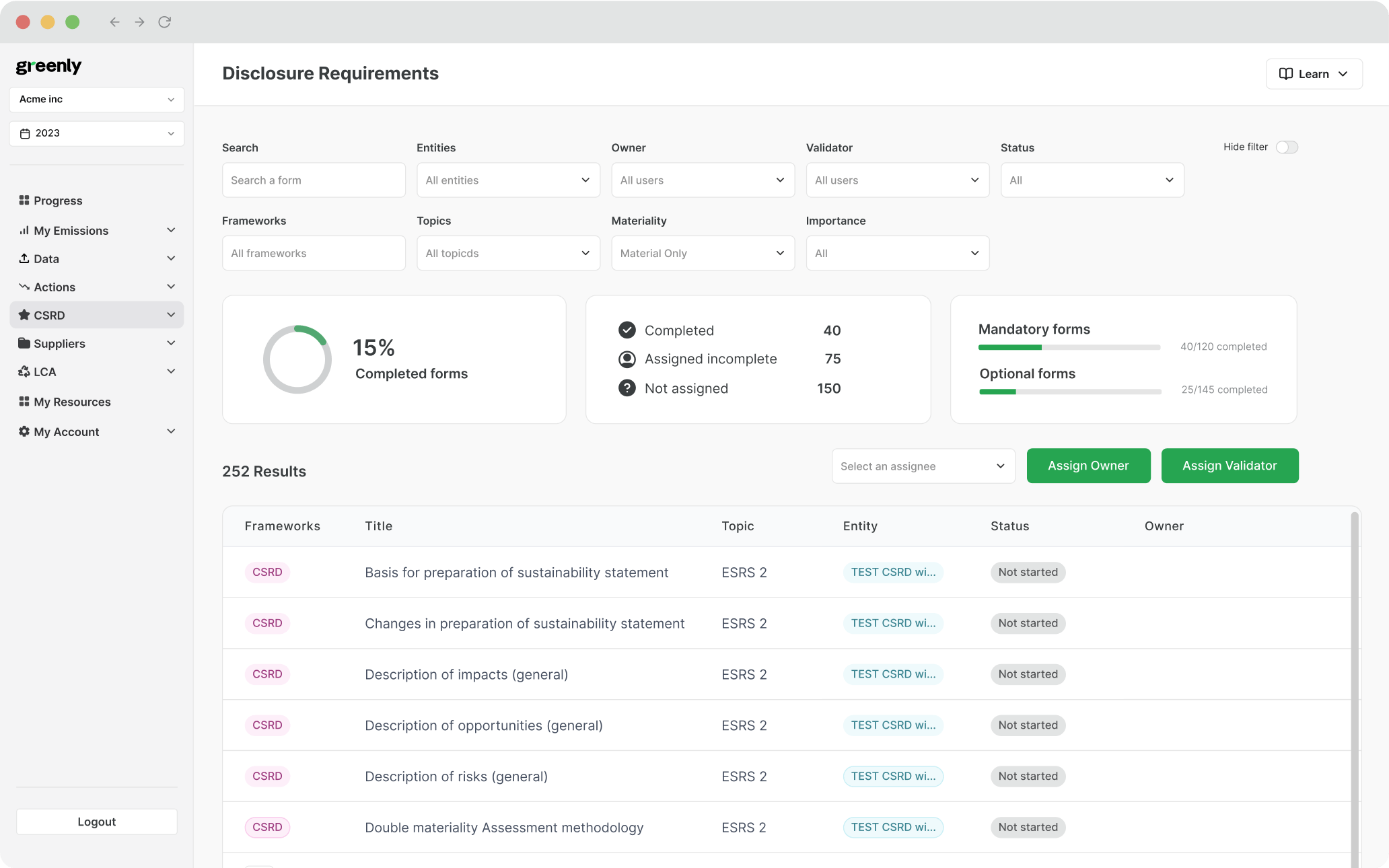

Mandates public and private corporations with over $1 billion in annual revenue to disclose their full greenhouse gas footprint (Scopes 1, 2, and 3).

ESG / CSR

Industries

MEASURE

ACT

COMFORM

California Climate Accountability Package: SB253, SB261, & SB252

Level

By Stephanie Safdie, US Copywriter, on 23/08/2023

Updated by Kara Anderson, on 22/05/2026

California has long been a global pioneer in environmental policy. As home to one of the largest economies in the world, the state’s landmark California Climate Accountability Package has fundamentally transformed how large corporations manage and report their environmental footprints.

By mandating rigorous corporate transparency, this suite of legislation aims to keep greenhouse gas (GHG) emissions at bay, standardise climate-related financial risk disclosures, and protect financial markets from the volatile impacts of a warming planet.

But what exactly is the California Climate Accountability Package, and how do Senate Bills 253, 261, and 252 work together to push businesses toward sustainable, transparent operations?

In this article, we'll cover:

The 2026 compliance landscape for SB 253 and SB 261

Mandated disclosure rules for Scope 1, 2, and 3 emissions

Corporate requirements for tracking climate-related financial risks

Fossil fuel divestment mandates under SB 252

What is the California Climate Accountability Package?

The California Climate Accountability Package is a groundbreaking suite of state legislation designed to transition corporate climate reporting from a voluntary, corporate social responsibility (CSR) exercise into a strict, legally binding mandate.

The package consists of three connected bills:

Requires companies with over $500 million in annual revenue to publicly disclose their climate-related financial risks and mitigation strategies.

Mandates that California’s massive public pension funds (CalPERS and CalBRS) completely divest from fossil fuel companies by 2031.

Clarifying SB 219: A common regulatory misconception is that a subsequent bill, SB 219, replaced or merged these laws. In reality, SB 219 was an administrative cleanup bill signed into law by Governor Gavin Newsom. It left the core mandates of SB 253 and SB 261 intact but altered the implementation mechanics - notably giving the California Air Resources Board (CARB) the flexibility to finalise the official reporting frameworks.

Driving transparency amidst federal rollbacks:

The fundamental goal of this package is to force corporate transparency regarding environmental footprints and financial vulnerabilities to climate change. This includes forcing companies to evaluate both physical risks (eg. operational disruptions from extreme weather) and transition risks (eg. the economic costs of shifting away from fossil fuels).

The local impact is massive, pulling thousands of large businesses operating in California into a strict compliance web overseen by CARB. However, its global impact is proving even more significant due to shifts in federal climate policy.

While the U.S. Securities and Exchange Commission (SEC) recently moved to formally rescind its federal climate disclosure rule in May 2026 following years of legal stays and a shift in leadership, California’s mandates have moved forward. CARB voted to adopt the initial implementing regulations for SB 253, effectively establishing California as the primary regulatory standard for climate disclosure in the United States.

By mirroring aspects of international standards like Europe’s Corporate Sustainability Reporting Directive (CSRD), the California Climate Accountability Package ensures that doing business in the world's 5th largest economy requires rigorous, auditable carbon accounting.

SB 253 & SB 261: Finalised timelines and the 2026 compliance reality

Navigating California’s climate legislation requires understanding the separation between emissions disclosure (SB 253) and climate financial risk reporting (SB 261). Following a landmark ruling by the California Air Resources Board (CARB) on February 26, 2026, the administrative rules, fee structures, and first-year deadlines have been officially locked in.

Crucially, the legal status of these two bills has diverged significantly due to recent federal court actions.

SB 253: The Climate Corporate Data Accountability Act (CCDAA)

SB 253 remains fully active and unaffected by ongoing industry litigation. If your corporation is a public or private U.S.-based entity "doing business in California" with total global annual revenues exceeding $1 billion, compliance is an immediate requirement.

The Phased Implementation Timeline

First-year reporting deadline. Covered entities must formally disclose their Scope 1 (direct operational emissions) and Scope 2 (indirect emissions from purchased electricity/heating) data based on their 2025 fiscal year.

Scope 3 (upstream and downstream supply chain emissions) reporting officially phases in, dragging a company's entire value chain into the disclosure net.

Third-Party Assurance

To combat greenwashing, CARB is phasing in independent audit requirements. Limited assurance for Scopes 1 and 2 will be required in the coming years, scaling up to strict reasonable assurance protocols by 2030.

SB 261: The Climate-Related Financial Risk Act

SB 261 targets corporations, partnerships, and business entities operating in California with total annual revenues of $500 million or more. It mandates biennial reporting aligned with the Task Force on Climate-related Financial Disclosures (TCFD) framework, detailing macro-level physical and transition climate risks.

The 2026 Legal Stay: "Stayed" Does Not Mean "Stopped"

While the statutory deadline for the first report was initially set for January 1, 2026, the current legal landscape has shifted:

The Ninth Circuit Injunction

The U.S. Court of Appeals for the Ninth Circuit issued a temporary injunction blocking the enforcement of SB 261 while a constitutional "compelled speech" lawsuit winds its way through the courts.

CARB's Current Stance

CARB has formally stated it will not penalise or enforce SB 261 mandates against covered entities while this judicial stay remains active.

The Voluntary Docket

Despite the pause, CARB opened an official public SB 261 reporting docket. Forward-thinking companies are proactively uploading their TCFD-aligned risk reports voluntarily to demonstrate market leadership and avoid a mad scramble if the injunction is lifted later this year.

Doing business in California:

Many multinational corporations mistakenly believe they are exempt if they lack a physical headquarters in the state. Under the California Revenue and Taxation Code applied by CARB, your entity is legally "doing business" in the state if it engages in any transaction for financial gain and meets inflation-adjusted thresholds:

California Sales ≥ $757,070

(for the 2025 tax year)

If your global revenue is over $1B (SB 253) or $500M (SB 261) and you cross this minimal sales threshold within state lines, you are legally required to comply.

Deep dive: SB 253 (The Climate Corporate Data Accountability Act)

The Climate Corporate Data Accountability Act (CCDAA), codified as SB 253, represents a tectonic shift in U.S. climate policy. By mandating emissions reporting across a company's entire value chain, the law successfully establishes a standardised, public database of corporate carbon footprints.

Who Qualifies under SB 253?

The qualification criteria for SB 253 are straightforward but highly encompassing. A business must meet two conditions to be considered an in-scope "reporting entity":

It must be a public or private partnership, corporation, or business entity formed under the laws of any U.S. state or the District of Columbia.

It must have total global annual revenues exceeding $1 billion USD while actively "doing business" in the state of California.

Because applicability is determined by global revenue—not just revenue generated within California boundaries—the law captures thousands of multinational conglomerates headquartered outside the state.

What Must Be Reported: The Three Scopes

SB 253 mandates that companies account for and report their emissions in strict alignment with the Greenhouse Gas Protocol (GHG Protocol). Reporting is broken down into three distinct tiers:

Scope 1 (Direct Emissions)

Greenhouse gas emissions originating directly from sources owned or operationally controlled by the company (e.g., corporate vehicle fleets, manufacturing plants, boilers, or refrigeration equipment).

Scope 2 (Indirect Emissions)

Emissions generated from the production of electricity, steam, heating, or cooling purchased and consumed by the reporting company.

Scope 3 (Value Chain Emissions)

All other indirect emissions that occur across the company’s upstream and downstream value chain. This spans 15 distinct categories under the GHG Protocol, including business travel, employee commuting, waste disposal, and third-party logistics.

The audit and assurance roadmap

To prevent greenwashing and guarantee data integrity for public financial markets, SB 253 introduces a phased independent verification mechanism. While CARB's finalised rules confirmed that third-party assurance is not required for the initial August 10, 2026 reporting window, a rigorous audit roadmap takes effect immediately afterward:

2027–2029 (Limited Assurance)

Reporting entities must obtain independent "limited assurance" verification for their Scope 1 and Scope 2 disclosures. This level of audit reviews methodologies and mathematical calculations to ensure no obvious errors exist.

2030 and Beyond (Reasonable Assurance)

The verification standard upgrades to "reasonable assurance" for Scopes 1 and 2—matching the rigorous depth of a traditional corporate financial audit.

The Scope 3 Audit Decision

CARB is mandated to review data quality separately. A final decision will be made by CARB on whether independent assurance will phase into Scope 3 value chain metrics by 2030.

Deep dive: SB 261 (The Climate-Related Financial Risk Act)

While SB 253 focuses on a company's structural impact on the environment, SB 261 turns the lens around, requiring companies to evaluate the environment's structural impact on their balance sheets.

Who qualifies under SB 261?

The net for financial risk reporting is cast twice as wide as the emissions mandate. SB 261 applies to public and private U.S. entities doing business in California with total annual global revenues exceeding $500 million USD.

Important institutional exemptions: Notably, insurance companies and businesses actively regulated by the California Department of Insurance are entirely exempt from SB 261, as they are already subject to distinct, highly specialised climate risk stress-testing frameworks.

Framework and alignment

In-scope corporations are required to draft and publish a comprehensive, biennial climate-related financial risk report. This disclosure must strictly align with the Task Force on Climate-related Financial Disclosures (TCFD) framework, International Financial Reporting Standards (IFRS S2), or an equivalent internationally recognised regulated standard.

Reports are required to transparently detail exposure across four core pillars:

Governance

The board’s oversight and management's role in assessing and managing climate-related risks and opportunities.

Strategy

The actual and potential impacts of climate-related risks on the organisation's businesses, strategy, and financial planning.

Risk Management

The structural organisational processes used to identify, assess, and mitigate climate liabilities.

Metrics and Targets

The specific indices used to assess and manage material climate risks.

Companies must specifically account for two types of climate threats:

Physical Risks

Direct threats to infrastructure, assets, and supply chains caused by severe, acute weather events (wildfires, flooding) or chronic shifts (sea-level rise, prolonged droughts).

Transition Risks

The economic, regulatory, technology, and reputational costs associated with migrating toward a low-carbon economy.

Reports must be made accessible to the public on the company's corporate website and formally filed to CARB’s digital registry. While the ongoing Ninth Circuit Court injunction means CARB is not currently enforcing penalties for missing files, the framework remains the benchmark for forward-looking risk modeling.

Deep dive: SB 252 (Public Retirement Systems: Fossil Fuel Divestment)

The final pillar of the original California Climate Accountability Package shifts focus away from private corporate mandates and directly targets the immense purchasing power of the state's public sector asset allocation.

The core mandate

Senate Bill 252 explicitly forbids California's premier public investment mechanisms - the California Public Employees’ Retirement System (CalPERS) and the California State Teachers’ Retirement System (CalSTRS) - from making any new investments or renewing existing contracts with carbon-intensive entities.

The scope of the bill explicitly zeroes in on the top 200 largest publicly traded fossil fuel companies, defined by the size of their oil, gas, and coal reserves.

The divestment and transition timeline

Because a sudden, reckless liquidation of assets could trigger significant financial shocks and violate fiduciary responsibilities to public workers, SB 252 outlines a highly methodical, multi-year transition horizon:

Portfolio Reviews

Pension boards must conduct comprehensive, transparent exposure audits to track exactly where capital is tied up in fossil fuel equity and debt.

Transition & Engagement Planning

CalPERS and CalSTRS are mandated to establish phased liquidation strategies that shift public capital away from fossil fuels and reallocate those funds into green investments and ESG-friendly asset classes.

2031 (Complete Divestment Target)

This marks the hard statutory deadline. By 2031, both public pension systems must completely liquidate all shareholdings, bonds, and direct private equity stakes in the identified carbon-intensive corporations.

While the bill faced substantial resistance in the Assembly during previous sessions, the push for state pension realignment continues to shape how public capital operates in the energy sector, serving as a legislative model for public funds across the country.

How to prepare with Greenly & EcoPilot AI

With CARB locking in the first corporate reporting window, large enterprises can no longer treat carbon accounting as a manual, spreadsheet-driven task. The sheer scale of data collection required for SB 253 compliance demands an automated, auditable approach.

To bridge this gap, Greenly has integrated EcoPilot AI directly into its carbon accounting platform, providing businesses with a streamlined, end-to-end tool to meet California’s rigorous data standards.

De-risking the August 10, 2026 milestone

For organizations scrambling to assemble their Scope 1 and Scope 2 greenhouse gas inventories for the August submission, EcoPilot AI dramatically shortens the data-gathering lifecycle, cutting overall assessment time by up to 80%.

Automated Data Ingestion

EcoPilot AI bypasses manual entry errors by automatically ingesting and organising corporate data - including utility invoices, fuel records, and operational footprints—instantly transforming raw documents into clean, categorized activity data.

AI-Powered Quality Control

Raw numbers are automatically mapped to verified emission factors using advanced machine learning models. The system instantly flags data anomalies and bridges information gaps, ensuring that your final Scope 1 and 2 tallies match the precision demanded by CARB.

ISO-Style Audit Trails

Under SB 253, data reliability is paramount. Every emission calculation performed by Greenly and EcoPilot AI retains an unalterable audit trail, providing the precise documentation required to sail through upcoming third-party limited assurance verification.

Solving the 2027 Scope 3 value chain challenge

While the immediate focus remains on Scopes 1 and 2, the true administrative bottleneck lies ahead in 2027, when Scope 3 supply chain reporting becomes mandatory. Tracking emissions across thousands of independent, global vendors is notoriously complex.

The Scope 3 edge: EcoPilot AI is built specifically to handle the data fragmentation of value-chain tracking. Operating via an intuitive conversational interface, it allows sustainability teams to automatically scale supplier engagement, screen entire supply chains in minutes rather than weeks, and accurately combine activity-based and spend-based calculation methods. This enables you to model your entire upstream and downstream footprint long before the 2027 legal mandates land.

Enterprise scenario analysis and risk readiness

Even though the Ninth Circuit Court has temporarily paused the enforcement of SB 261 risk reports, forward-thinking market leaders are not standing still. Greenly provides the continuous data centralisation needed to build out your TCFD-aligned risk frameworks ahead of time.

Through the platform, compliance teams can execute robust climate scenario analysis to model both physical risk exposure (like infrastructure vulnerability to severe weather) and transition risk pathways. Keeping these disclosure datasets updated and ready ensures that the moment judicial stays are lifted, your mandatory biennial report can go live with a single click.

By utilising EcoPilot AI, companies can effectively transform what feels like a complex, shifting regulatory burden into a streamlined exercise in strategic corporate resilience.

Frequently Asked Questions

Can a parent company submit a single consolidated climate report for its subsidiaries?

Yes, under the final CARB regulations, parent companies are explicitly permitted to file a single, consolidated disclosure at the corporate group level. If a parent company files a comprehensive report that covers all emissions and financial risks of its umbrella organisations, any underlying subsidiaries that independently meet the revenue thresholds are exempt from filing separate, individual reports. However, businesses should note that CARB's administrative fees are calculated on a per-entity flat fee basis, meaning the total fee invoiced for a consolidated report will scale based on the number of in-scope subsidiaries it covers.

What are the penalties for non-compliance with SB 253 or SB 261?

Failing to comply with California's climate mandates carries steep administrative penalties, capped at $500,000 USD per year for SB 253 violations and $500,000 USD per reporting cycle for SB 261. While CARB has the authority to issue daily fines of up to $2,500 for missing or inadequate reports, the agency has formally committed to using maximum enforcement discretion and leniency for good-faith first-year submissions. Furthermore, because of the active Ninth Circuit Court injunction blocking SB 261 enforcement, no financial penalties can be assessed for climate risk reporting until the active judicial stay is legally resolved.

Are non-profit organisations or charities required to comply with these climate laws?

No, tax-exempt non-profit organisations, charities, and public government entities are completely exempt from the reporting requirements of both SB 253 and SB 261. Even if a non-profit organisation's gross global receipts exceed the $500 million or $1 billion thresholds, CARB’s finalised regulatory framework explicitly excludes entities that operate under non-profit tax status from the definitions of a covered reporting entity. The mandates are strictly restricted to traditional commercial partnerships, corporations, and limited liability companies (LLCs) structured for financial gain.

How does California define global annual revenue to determine who must report?

To eliminate corporate ambiguity and streamline verification, CARB’s finalised framework specifies that a company's total annual revenue is determined by its total gross receipts as reported to the California Franchise Tax Board (FTB) or equivalent federal tax filings. This gross revenue calculation evaluates total global inflows without reductions for the cost of goods sold (COGS) or the basis of property sold. If this macro-level gross receipt number crosses the statutory thresholds in your previous fiscal year, your business is legally locked into the compliance tier.

Is independent third-party auditing required for the 2026 reporting cycle?

No, third-party assurance or independent verification is not required for the initial August 10, 2026 reporting window under SB 253. Under CARB's phased implementation strategy, the first reporting cycle allows companies to submit self-certified Scope 1 and Scope 2 data based on internal metrics. The requirement for independent auditing officially begins in 2027, introducing a mandatory "limited assurance" verification standard that will eventually elevate to a highly rigorous reasonable assurance framework by 2030.

What About Greenly?

Streamlined ESG Data Management & Compliance

Greenly streamlines the complex process of ESG data collection, consolidation, and management all in 1 platform.

📥 Import qualitative & quantitative data — platform processes & flags errors

🤖 AI-powered data processing & auto-filling of answers

🔗 Integrated connectivity: map & connect data points across indicators, eliminate redundancy

📂 Centralised platform for all ESG data & supporting docs

⏱️ Track collaborator progress, set reminders & deadlines for compliance

🛡️ Audit-ready traceability: instantly track every change

📊 ESG dashboards to track all key KPIs

🏢 Multi-entity task management & data ingestion at all levels

🧠 AI-powered pre-filling from documentation saves weeks of manual work

🧮 Automatic calculations handle dependencies & speed up consolidation

📈 Multi-entity data collection simplified by mirroring company structure

Strategic ESG Impact & Risk Mitigation

Greenly empowers companies to move beyond reporting to develop strategy, identify risks, and unlock opportunities.

📋 Automated Double Materiality Assessment (DMA) built with CSRD experts

🤖 AI-powered climate risk forecasting integrated into DMA with site-level detail

💰 Translate climate risk into quantified financial opportunities

📍 Location-specific financial risk breakdowns with IPCC-backed data

🔎 Data gap analysis from DMA to improve future reporting

📈 Automated Climate KPI integration

📊 Advanced Materiality Module: benchmarks & specialised add-ons (e.g., CSA)

Tailored & Future-Ready Reporting

Flexible reporting with interoperability across 15+ frameworks.

📝 Custom framework creation with tailored reports

🔀 Interoperability across 10+ frameworks with harmonised database

⚡ Accelerated report creation with AI-powered generation and pre-filling

📄 Auto-generation of complete ESG reports (qualitative & quantitative data)

🛡️ Audit-ready guaranteed reports

💻 Automated ESG report generation including XHTML & XBRL for CSRD

📂 Centralised audit trails & attachments per indicator

🤝 Collaborative workflows managing full indicator lifecycle

Expert Guidance & Continuous Support

Comprehensive support & training to empower ESG teams and ensure successful, autonomous reporting.

🧑💼 Dedicated Project Managers & ESG Experts for each framework

📚 Extensive training & resources available on the platform

🤖 AI-powered in-app chatbot (24/7) for instant answers

Share this article

Subscribe to the CSO Connect Newsletter

We care about your data in our privacy policy.

More articles

View all

Decarbonisation: what it is and why it matters

1 min

Level

What is decarbonisation and why is it urgent? Learn practical steps companies can take to support the global move toward net zero emissions.

Impacts, Risks, and Opportunities (IRO) for CSRD Reporting

1 min

Level

In this article, we’ll break down what IROs are, how to identify and assess them, and what CSRD requires in terms of disclosure.

The Carbon Border Adjustment Mechanism (CBAM)

14 min

Level

In this article, we break down what the EU CBAM is, how it works, and what businesses need to do to comply.