Greenlyhttps://www.greenly.earth/https://images.prismic.io/greenly/43d30a11-8d8a-4079-b197-b988548fad45_Logo+Greenly+x3.pngGreenly, la plateforme tout-en-un dédiée à toutes les entreprises désireuses de mesurer, piloter et réduire leurs émissions de CO2.Greenlyhttps://www.greenly.earth/Greenly, la plateforme tout-en-un dédiée à toutes les entreprises désireuses de mesurer, piloter et réduire leurs émissions de CO2.Descending4

“Double materiality sits at the core of the EU’s Corporate Sustainability Reporting Directive (CSRD), which came into effect on January 1, 2024. ”

It’s a key concept that asks companies to look at sustainability from two angles: how it affects them financially, and how their own activities impact people and the planet.

Since this dual lens is central to CSRD compliance, getting to grips with it isn’t just helpful, it’s essential.

In this article, we'll explore everything you need to know about the CSRD's double materiality assessment and practical steps for conducting it.

Close

What is a double materiality assessment?

The double materiality assessment is a cornerstone of the CSRD, requiring companies to evaluate sustainability from two key perspectives:

Financial Materiality (Outside-In): Examines how environmental and social factors, such as climate change or resource scarcity, affect the company’s financial performance and economic position. This financial perspective ensures that businesses account for sustainability risks that could impact their bottom line or long-term value.

Impact Materiality (Inside-Out): Evaluates how a company's operations and activities impact the environment, society, and broader stakeholders, such as through emissions or labor practices.

“This dual approach ensures companies provide a comprehensive view of their sustainability risks, impacts, and opportunities, aligning financial performance with broader sustainability considerations. ”

It builds on the traditional concept of single materiality, which focuses solely on financial risks and opportunities, to include the wider consequences of business activities.

Note: the Corporate Sustainability Reporting Directive (CSRD) is the EU’s new framework for corporate sustainability disclosure. It replaces the Non-Financial Reporting Directive (NFRD) and significantly raises the bar for what companies need to report, both in terms of scope and depth.

Note: The European Commission has proposed an Omnibus package that could reshape the CSRD’s scope and timelines. The goal is to align it more closely with the Corporate Sustainability Due Diligence Directive (CSDDD) and ease the burden on businesses. This is still just a proposal. It needs approval from both the European Parliament and the Council of the EU, and changes aren’t expected to take effect before 2027 at the earliest.

“Bottom line? Keep preparing under the current CSRD rules – it’s better to be ready than caught off guard.”

Double materiality and the CSRD

“The CSRD mandates that companies conduct a double materiality assessment to determine which sustainability topics - across environmental, social, and governance (ESG) areas - are materially relevant for reporting.”

While the directive does not prescribe a specific method, it outlines general guidelines:

💶

For financial materiality: Companies must evaluate the significance, importance, and likelihood of external factors influencing their financial stability.

🔍

For impact materiality: Businesses need to assess the quality, severity, and probability of their impacts on the environment and society.

Materiality Type

Focus

Key Question

Examples

Financial Materiality (Outside-In)

How external sustainability factors impact the company’s financial health

How could environmental or social issues affect our business performance?

- Climate change disrupting supply chains

- Carbon pricing increasing operational costs

- Water scarcity affecting production

Impact Materiality (Inside-Out)

How the company’s activities affect people and the environment

How do our operations impact the environment and society?

- Greenhouse gas emissions

- Labour practices in the supply chain

- Impacts on local biodiversity

Under the CSRD, companies must report in line with the European Sustainability Reporting Standards (ESRS), which include two cross-cutting standards and ten topical standards across environmental, social, and governance (ESG) topics.

“While some disclosures are mandatory for all companies, others depend on the results of a double materiality assessment to determine their relevance, including entity-specific sustainability matters unique to each organisation's operations and impacts.”

Key disclosures include:

💶

General Requirements (ESRS 1): Framework for reporting, covering governance, strategy, risk management, and climate-related metrics.

🔍

General Disclosures (ESRS 2): High-level information on impacts, risks, and opportunities, as well as governance and strategy.

Companies are expected to provide detailed disclosures on these topics where deemed materially relevant, aligning with global frameworks like the TCFD and ISSB.

This holistic approach reflects the growing demand for transparency and accountability, ensuring corporate reporting aligns with the EU's sustainability goals and supports better decision-making for all stakeholders.

The concept of double materiality is closely aligned with principles established by the Global Reporting Initiative (GRI), which has long emphasised the importance of considering both financial and non-financial impacts in corporate reporting. By incorporating these broader perspectives, double materiality ensures that reporting reflects the interconnectedness of business operations and sustainability issues.

How does double materiality align with other frameworks?

Many companies are already familiar with sustainability frameworks like the Global Reporting Initiative (GRI) or the International Sustainability Standards Board (ISSB), but the CSRD introduces a unique requirement by combining both financial and impact perspectives through its double materiality approach.

Here’s how the CSRD compares to other major frameworks:

CSRD

Double materiality

ISSB (IFRS S1 & S2)

Financial materiality only

GRI Standards

Impact materiality only

CSRD

Inside-out (impact) & Outside-in (financial)

ISSB (IFRS S1 & S2)

Outside-in: effect on enterprise value

GRI Standards

Inside-out: impact on people and the planet

CSRD

Comprehensive reporting required by European legislation

ISSB (IFRS S1 & S2)

Transparency aimed at investors and financial markets

GRI Standards

Reporting focused on stakeholders

“The CSRD essentially bridges the gap between the ISSB and GRI by requiring companies to report on both financial and non-financial impacts. For businesses already using one of these frameworks, the CSRD may feel familiar, but it requires a broader, more integrated approach. ”

Why does double materiality matter?

“Double materiality goes beyond traditional risk management by encouraging companies to look both inward and outward, identifying not just how sustainability affects the business, but also how the business affects the world around it. ”

This dual perspective matters because it:

Reveals the full picture of risk and impact – helping companies manage both external threats and their own operational footprint.

Enables more informed, long-term decision-making – by integrating sustainability into strategy, not just compliance.

Builds stakeholder and investor trust – with transparent, relevant reporting that reflects real-world concerns.

Supports EU sustainability goals – aligning corporate behaviour with the transition to a greener, fairer economy.

In short, double materiality is a mindset shift that supports better business and a more sustainable future.

How to conduct a double materiality assessment

Conducting a double materiality analysis is a comprehensive process that involves several steps to ensure accurate and meaningful sustainability reporting. Below is a detailed guide on how companies can carry out this assessment.

Step 1: Understand Context and Value Chain

Approach: Start by mapping your company's value chain and identifying key stakeholders involved in both upstream and downstream activities. Utilise existing sustainability documents, climate risk assessments, and human rights due diligence reports. This involves:

Reviewing the company's website and external materials for relevant information.

Considering the legal and regulatory environment.

Analysing media reports and publications about the company and its industry.

Looking at peer reports and sector-specific benchmarks.

Reviewing publications on sustainability trends and scientific findings.

Example: A food manufacturing company might map its value chain from raw material suppliers to end consumers, identifying key stakeholders such as farmers, transporters, retailers, and consumers.

Step 2: Propose Topics

Approach: Create a comprehensive list of potentially relevant sustainability matters using the ESRS topic list, industry reports, sustainability frameworks, and competitor analysis. This list should include both sector-agnostic and entity-specific matters.

Sector Topics: Use the ESRS list to identify general sustainability matters.

Entity Topics: Consider unique issues such as company-specific tax policies or unique operational impacts.

Example: A car manufacturer may list topics like emissions, energy use, labor practices, and product safety.

Step 3: Engage Stakeholders

Approach: Engage with stakeholders through surveys, focus groups, and interviews to gather feedback on the proposed topics. This should include internal and external stakeholders such as employees, suppliers, customers, investors, and community groups.

Methods of Engagement: Use varied methods like online surveys, in-person focus groups, and detailed interviews.

Example: A tech company might survey employees about workplace conditions, interview suppliers about labor practices, and hold focus groups with consumers about product impacts.

Step 4: Finalise Topics

Approach: Refine the list of ESG topics based on stakeholder feedback. Prioritise topics by their significance to stakeholders and impact on the business.

Collaboration: Work with key internal decision-makers to finalise the list.

Example: A pharmaceutical company might prioritise topics such as drug safety, access to medicines, and research ethics based on feedback from healthcare professionals, patients, and regulatory bodies.

Step 5: Identify IROs (Impacts, Risks, and Opportunities)

Approach: Conduct a detailed analysis for each prioritised topic to identify specific impacts, risks, and opportunities. This involves:

Impact Analysis: Identifying positive and negative impacts on people and the environment.

Risk Analysis: Assessing risks to the company's operations, reputation, and potential direct financial repercussions from sustainability-related issues.

Opportunity Analysis: Identifying opportunities for innovation and competitive advantage.

Example: A clothing retailer might identify the environmental impact of textile production, the risk of supply chain disruptions, and opportunities for sustainable sourcing practices.

Step 6: Score IROs

Approach: Develop a consistent scoring system based on the severity and likelihood of each IRO. Use both qualitative and quantitative data to score the IROs.

Scoring Criteria: Consider factors such as scale, scope, irremediable character, likelihood, and financial magnitude.

Example: A utility company might score the impact of carbon emissions, considering regulatory fines (severity) and the probability of increased regulation (likelihood).

Step 7: Assess Results

Approach: Aggregate and analyse scoring results to set thresholds for determining material topics. Document the rationale for these decisions to ensure transparency.

Setting Thresholds: Use both qualitative and quantitative thresholds to determine materiality.

Example: A mining company might set a threshold for water usage impacts based on regional water scarcity and stakeholder concerns.

Step 8: Integrate ESRS Disclosures

Approach: Align identified material topics and IROs with corresponding ESRS metrics and disclosures.

Data Integration: Ensure that the data collected aligns with ESRS reporting requirements and supports comprehensive disclosure.

Example: A financial institution might integrate climate risk data with ESRS disclosures on financial performance and risk management.

“Following these detailed steps ensures a robust double materiality assessment, helping companies identify and report all relevant sustainability topics. This process not only ensures compliance with the CSRD but also enhances transparency, stakeholder engagement, and strategic decision-making.”

Close

What about assurance?

Under the CSRD, sustainability information won’t just be reported, it will also need to be externally assured.

Starting from the first reporting year, companies must obtain limited assurance over their sustainability disclosures, including the results of their double materiality assessment.

In the coming years, this will shift to reasonable assurance, a higher level of scrutiny more comparable to financial audit standards.

“This makes it all the more important for companies to conduct a thorough materiality assessment, with well-documented processes and clear decision-making criteria.. Inaccurate or poorly documented processes won’t just affect reporting quality, they could create compliance risks and damage trust with investors, auditors, and regulators.”

Double materiality challenges

Carrying out a double materiality assessment isn’t always straightforward.

From collecting reliable data to aligning with evolving regulations, businesses face a number of practical hurdles along the way.

Below, we break down some of the key challenges, why they matter, and how to address them effectively:

Challenge

Why it matters

Solution

Data collection and analysis

Capturing reliable data across the full value chain is time-consuming, complex, and often involves inconsistent or incomplete inputs.

Use robust data management systems and advanced analytics to streamline processes and improve accuracy.

Engaging diverse stakeholders

Gaining meaningful input from a wide range of stakeholders is essential for credible reporting, but coordinating this can be difficult.

Create a structured engagement plan using surveys, interviews, and focus groups to ensure inclusive feedback.

Defining materiality thresholds

Materiality can be subjective, and unclear thresholds risk missing key issues or including irrelevant ones.

Set clear criteria based on both qualitative and quantitative data, aligned with industry standards and stakeholder expectations.

Ensuring consistency and standardisation

Disparate systems across regions or business units can lead to inconsistent reporting and reduced credibility.

Develop internal guidelines and standardised processes to ensure reliable data across the organisation.

Keeping up with regulatory changes

Sustainability regulations are evolving quickly, and falling behind can mean non-compliance or reputational risk.

Monitor developments continuously and adapt internal processes to remain aligned with new requirements.

Integrating with strategic planning

If insights from the assessment aren’t embedded into business strategy, the process risks becoming a box-ticking exercise.

Align ESG goals with overall business objectives and embed sustainability into key decision-making frameworks.

“Navigating the complexities of double materiality and CSRD reporting can be particularly challenging for companies. The process demands extensive data collection, engaging diverse stakeholders, balancing financial and impact materiality, and staying updated with evolving regulations. Each step requires meticulous planning and execution to ensure compliance and transparency. These challenges can be daunting, making it essential for companies to have expert guidance.”

That's where Greenly comes in. Greenly offers comprehensive CSRD reporting services to help companies effectively manage these complexities, ensuring accurate and compliant sustainability reporti

Close

How Greenly can help your company with CSRD reporting

Greenly can help your company comply with the Corporate Sustainability Reporting Directive (CSRD), utilising a Double Materiality Methodology to ensure thorough, accurate, and streamlined reporting. Our platform offers a range of features designed to help your organisation manage, assess, and report on sustainability metrics effectively. Here's how Greenly can assist you:

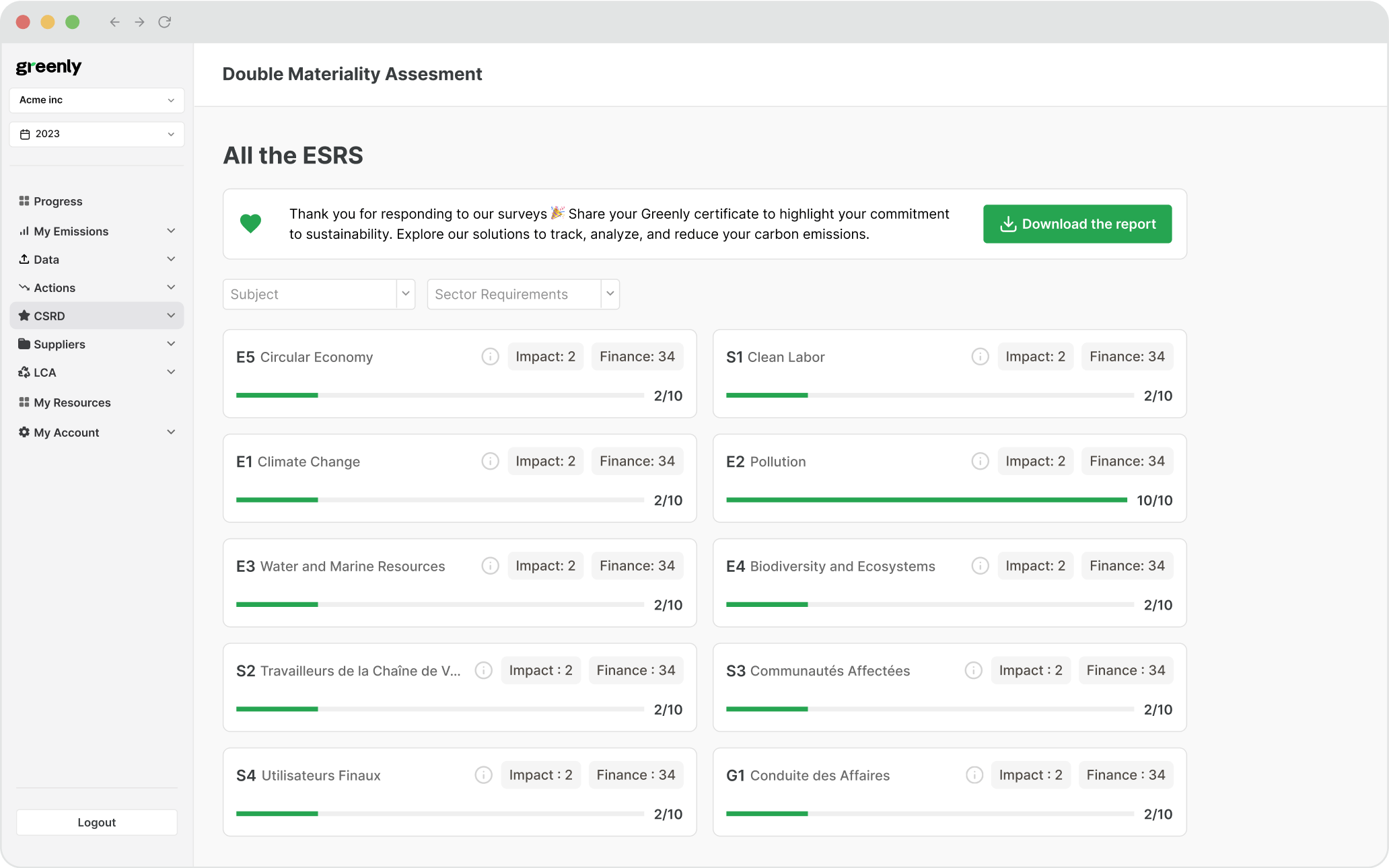

Double Materiality Assessment

Greenly employs a form-based approach to streamline the process, essential for CSRD compliance. This method helps identify significant impacts, risks, and opportunities related to your company's activities, products, and services.

Form-based Assessment: Structured forms aligned with thematic ESRS requirements capture a comprehensive picture of your company's sustainability impacts. These forms are tailored to each major sustainability topic, ensuring that only material IROs are included in your CSRD report.

Engagement and Accessibility: Our platform integrates comment boxes throughout the forms, allowing for additional context and details, and ensuring a customised and thorough assessment.

Impact and Financial Materiality: Assess both the environmental and financial impacts of your activities. Quantify the severity, scope, remediability, and likelihood of impacts, and evaluate financial consequences to determine significant risks and opportunities.

Onboarding and Training

Greenly provides extensive onboarding and training to ensure you are fully equipped to navigate the CSRD framework.

Comprehensive Training Materials: Detailed documents covering the CSRD process, including data collection guidelines and reporting obligations, are available in our Help Center.

Interactive Training Sessions: These sessions encourage discussion and feedback, ensuring all participants thoroughly understand the material and their responsibilities.

Data Collection and Reporting

Our platform facilitates efficient data collection and reporting, essential for CSRD compliance.

Integration and Format Compliance: Ensure all data meets CSRD formatting requirements, whether integrated from Greenly's platform or transferred from your internal systems.

Project Management Tools: Manage the data collection process with features that include descriptions of data points and data extraction formats.

Data Storage and Retrieval: Simplify future reporting cycles with effective data retrieval systems and proof management.

Task Management & Progress Monitoring: Monitor your reporting progress in real-time, ensuring timely completion and accountability.

Advanced Features

Greenly's platform offers advanced features to enhance your reporting.

Carbon Reduction Simulation: Assess the potential impact of your carbon reduction plans using our simulation tools.

Audit-Ready Platform: Built with security at its core, our platform ensures your data is protected and audit-ready, enhancing the credibility of your reports.

Ease of Access for Auditors: Simplify the audit process with straightforward access for auditors to review and verify data directly on the platform.

Automatic Export: Generate and export your sustainability reports in the required XHTML format with XBRL tagging to meet all technical specifications.

By partnering with Greenly, your company can confidently incorporate double materiality and navigate the complexities of CSRD compliance, ensuring that your sustainability reporting is comprehensive, accurate, and aligned with regulatory requirements.

“Greenly not only offers support for CSRD compliance, we also provide a suite of carbon management solutions to support businesses in reducing their environmental impact and meeting sustainability goals.”

By focusing on actionable strategies and cutting-edge tools, Greenly empowers companies to take control of their emissions and align with global climate objectives.

Carbon Management: Greenly's platform simplifies the process of tracking carbon emissions across all scopes: direct (Scope 1), indirect (Scope 2), and supply chain-related (Scope 3). By accurately measuring emissions at every level, companies can identify high-impact areas and take meaningful steps to reduce their overall carbon footprint.

Tailored Emissions Reduction Plans: Beyond measurement, Greenly provides practical insights and recommendations to help companies reduce emissions. From energy usage and transportation to waste management and operational efficiency, Greenly's science-based action plans guide businesses toward impactful changes that align with their sustainability goals.

Lifecycle Assessments (LCAs): Greenly helps businesses assess the carbon impact of their products and services across their entire lifecycle. By understanding the footprint of every stage - from raw material sourcing to end-of-life disposal - companies can make informed decisions to improve sustainability.

Building a Sustainable Supply Chain: Supply chain emissions (Scope 3) often account for the largest share of a company's carbon footprint. Greenly offers tools to evaluate and mitigate these emissions, providing insights into supplier practices and supporting sustainable procurement. By working with aligned suppliers, companies can reduce emissions while building resilience across their supply chain.

Offsetting Residual Emissions: For emissions that cannot yet be reduced, Greenly connects companies with verified carbon offset projects. From reforestation efforts to renewable energy initiatives, these projects support global climate action and help businesses address their residual impact responsibly.

“Greenly empowers companies to take actionable steps toward sustainability. With effective carbon management solutions, tailored reduction plans, and tools to build a resilient supply chain, your business can make a meaningful difference.”