Decarbonization: what it is and why it matters

1 min

Level

What is decarbonization, and why is it urgent? Learn practical steps companies can take to support the global move toward net zero emissions.

ESG / CSR

Industries

By Kara Anderson, UK Copywriter, on 08/24/2023

Updated by Kara Anderson, on 03/11/2026

To prevent companies from evading climate regulations by relocating production to countries with laxer standards, the EU has introduced the Carbon Border Adjustment Mechanism (CBAM), a tool designed to level the playing field and curb carbon leakage.

This initiative addresses an important concern: approximately 23% of global CO₂ emissions are embedded in traded goods - meaning nearly a quarter of emissions - are tied to products manufactured in one country and consumed in another.

A transitional phase kicked off in October 2023, introducing new reporting requirements for importers of certain carbon-intensive goods.

While the definitive CBAM system begins in 2026, the first financial settlement will take place in 2027, when importers submit their first annual declaration and surrender CBAM certificates for 2026 imports.

Companies need to start preparing now - including businesses outside the EU.

What the CBAM is and how it fits into the EU’s climate strategy

Why the mechanism was introduced, including the problem of carbon leakage

How it works – including timelines, reporting rules, and what products are affected

What changes to expect after 2026, including carbon pricing and penalties

Who the CBAM applies to

What businesses need to do to prepare, and how Greenly can help support compliance

As the EU tightens its climate policies through instruments like the Emissions Trading System (EU ETS), there’s been growing concern about carbon leakage.

To address this, the CBAM places a carbon price on certain imported goods to reflect the emissions released during their production. In other words, it ensures that imported products face the same carbon costs as those made within the EU.

This is particularly relevant given that imports of carbon-intensive goods into the EU account for over 20% of the EU’s total emissions.

CBAM adopted – 10 May 2023

The EU adopted the Carbon Border Adjustment Mechanism as Regulation (EU) 2023/956.

The transitional phase began on 1 October 2023, with detailed reporting rules adopted through an implementing regulation on 17 August 2023.

Transitional reporting period – October 2023 to December 2025

During this phase, EU importers were required to report the embedded greenhouse gas emissions of CBAM-covered goods on a quarterly basis.

The final transitional report (covering Q4 2025 imports) was due on 31 January 2026.

Definitive phase begins – 1 January 2026

CBAM has now entered its definitive phase. Importers must register as authorized CBAM declarants and comply with the full regulatory framework.

The first annual declaration and certificate surrender will take place in 2027, covering emissions embedded in goods imported during 2026.

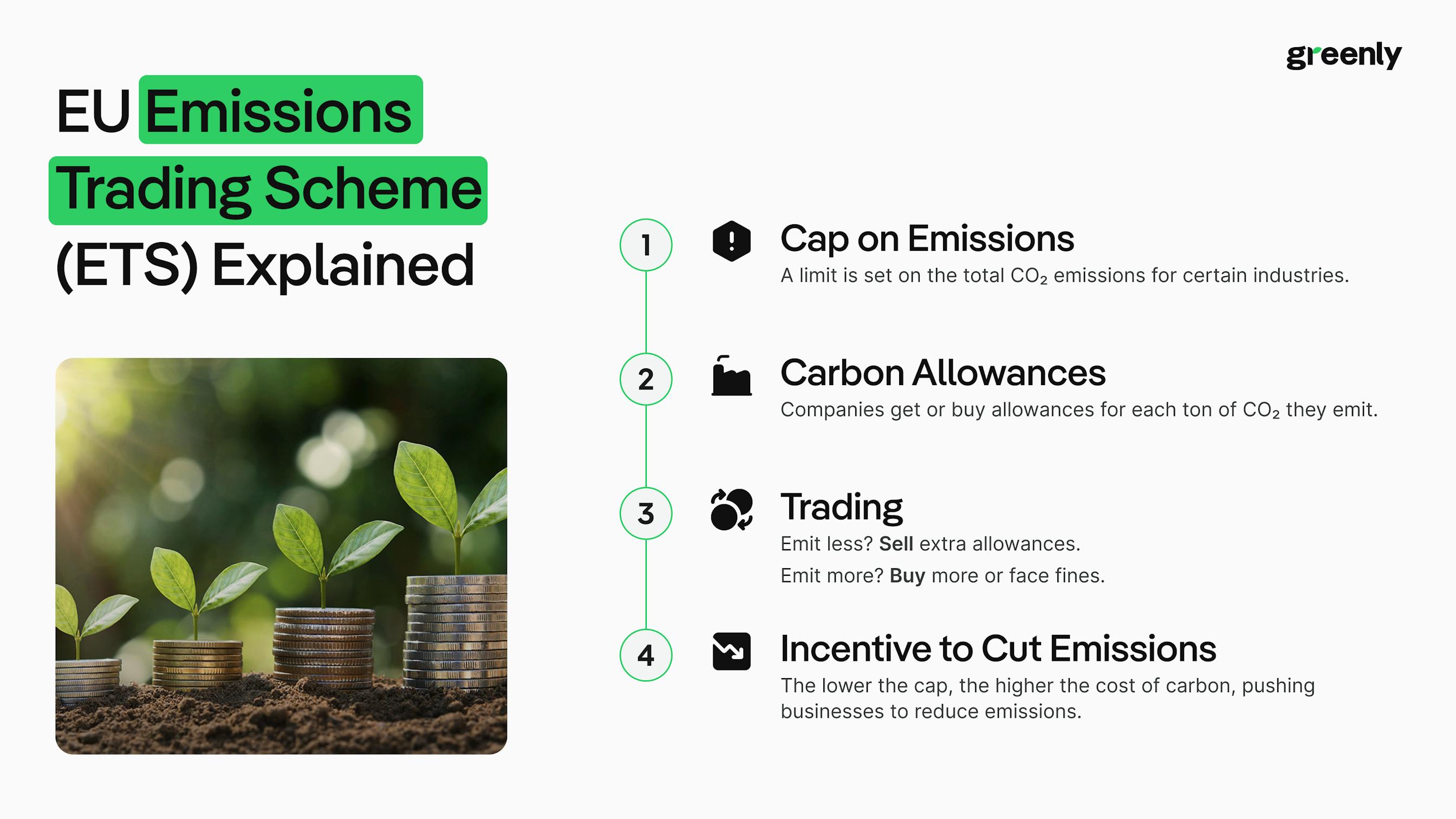

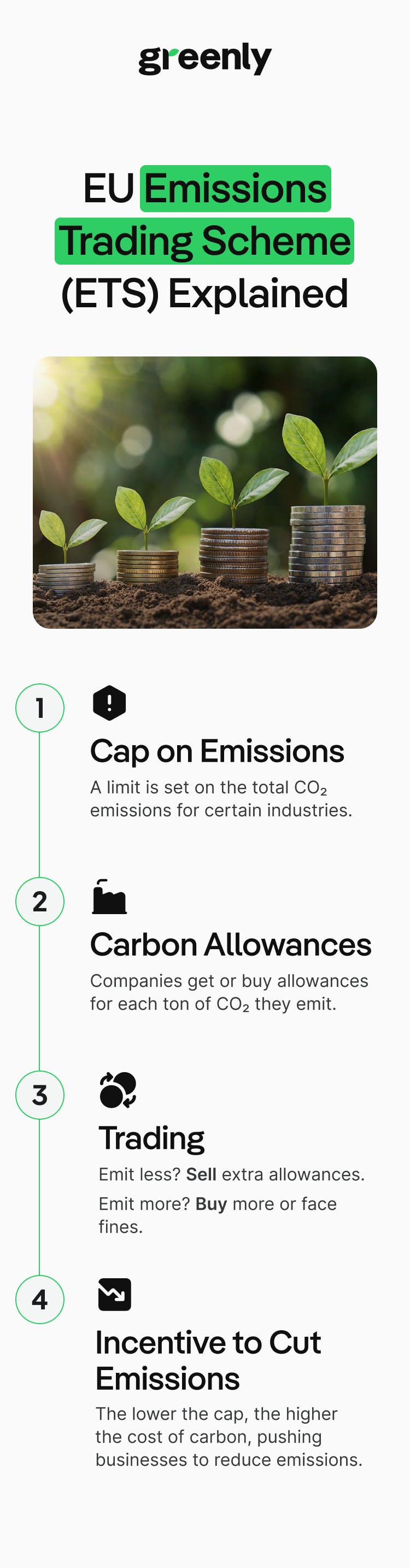

The ETS is the world’s first and largest carbon market and works by putting a price on carbon. It sets a cap on the total amount of CO2 that can be emitted by certain sectors each year, and companies must hold carbon allowances to match their emissions.

Over time, the emissions cap is reduced, increasing the pressure to decarbonise.

To support the EU industry during the early years of the scheme, free allowances were granted to certain energy-intensive sectors. However, these are being phased out between 2026 and 2034 to ensure the system continues to drive emissions reductions.

Carbon leakage occurs when companies move their production to countries with weaker climate policies to avoid the costs of carbon pricing, or when lower-cost, high-emission imports replace EU-made products.

The result? Emissions are simply outsourced, not reduced.

As the European Commission explains:

Because the ETS only applies within the EU, it can’t prevent emissions shifting across borders. Research by the European Central Bank has shown that some companies have already relocated their most carbon-intensive operations outside the EU, undermining the impact of the ETS.

To address this loophole, the EU proposed the Carbon Border Adjustment Mechanism on 14 July 2021 as part of the “Fit for 55” climate package. The goal? To apply a carbon price - similar to a carbon tax - to imported goods from countries not covered by the ETS, and ensure that EU climate efforts aren’t undercut by cheaper, more polluting products made abroad.

The Carbon Border Adjustment Mechanism (CBAM) requires importers to account for the greenhouse gas (GHG) emissions embedded in certain carbon-intensive goods they bring into the EU.

These emissions are tied to how the goods were produced, whether entirely or partially outside the EU, and will soon carry a carbon cost, similar to what EU producers already face under the Emissions Trading System (ETS).

CBAM applies to EU-based importers of specific goods produced outside the EU or in countries not covered by the EU ETS.

This includes:

Yes - to reduce the administrative burden on smaller importers and specific trade scenarios, the CBAM includes several targeted exemptions during the transitional phase.

These may evolve over time as the mechanism matures.

| Exemption | Description |

|---|---|

|

Low-value consignments

|

Shipments with a total intrinsic value under €150 are exempt from reporting obligations during the transitional period. |

|

Returned goods

|

Goods re-imported into the EU without modification after export are not subject to CBAM. |

|

Outward processing

|

Goods processed outside the EU and re-imported under the outward processing customs procedure are exempt. |

|

De minimis volume threshold

|

In 2025, the EU formally adopted a simplification package introducing a 50-tonne annual de minimis exemption for certain CBAM goods (including iron and steel, aluminum, cement, and fertilizers). Importers bringing in less than 50 tonnes per year are exempt from CBAM obligations. The measure aims to reduce administrative burden for small importers while still covering more than 99% of embedded emissions from CBAM sectors. |

To allow businesses time to adapt, the EU introduced CBAM in two stages. The transitional phase ran from 1 October 2023 to 31 December 2025 and was designed to familiarize importers with the system before the financial mechanism took effect.

During this period, EU importers of certain carbon-intensive goods were required to report the greenhouse gas emissions embedded in their imports, but they did not yet have to purchase CBAM certificates. The goal was to collect emissions data, build reporting infrastructure, and give businesses time to establish processes for gathering information from suppliers.

During the final year of the transitional phase, the EU also tightened reporting rules. From 1 January 2025, importers were required to use the EU methodology for calculating embedded emissions, replacing earlier simplified approaches used during the early reporting period.

The transitional phase helped the EU gather emissions data and prepare the administrative systems needed for full CBAM implementation. From 1 January 2026, the mechanism entered its definitive phase. Importers must now register as authorized CBAM declarants and comply with the full regulatory framework, with the first certificate surrender scheduled for 2027 to cover emissions from goods imported in 2026.

From 1 January 2026, the Carbon Border Adjustment Mechanism entered its definitive phase. This marks the transition from the reporting-only transitional period to the full CBAM regulatory framework.

However, the first financial settlement will take place in 2027, when importers submit their first annual CBAM declaration and surrender certificates covering emissions from goods imported during 2026.

At this point:

To comply with the definitive CBAM regime, importers must also purchase and hold CBAM certificates corresponding to the emissions embedded in their imports. During the year, importers are generally required to maintain a number of certificates corresponding to at least 80% of the embedded emissions in their imported goods.

The price of CBAM certificates is linked to the price of allowances in the EU Emissions Trading System (EU ETS). During 2026, certificate prices are published based on the quarterly average ETS auction price, before moving to a weekly price calculation from 2027 onwards. This ensures the carbon cost of imported goods reflects the carbon price paid by EU producers.

If an importer can prove that a carbon price has already been paid in the country of production, this amount can be deducted from their CBAM obligation to avoid double carbon pricing.

These obligations will increase financial exposure for many businesses. At the same time, free allowances under the EU ETS will begin phasing out from 2026 and are scheduled to disappear completely by 2034, meaning the effective carbon cost for many industrial sectors will gradually rise.

This creates a strong financial incentive, not only for importers but also for their international suppliers, to reduce the emissions intensity of their products and invest in cleaner production methods.

In February 2025, the European Commission introduced a set of proposed changes to the Carbon Border Adjustment Mechanism (CBAM) as part of its first Omnibus simplification package. The goal was to streamline the system, reduce administrative burdens, and make compliance more manageable for businesses, particularly smaller importers.

These simplifications were adopted later in 2025 and are now part of the CBAM regulatory framework.

Key measures include:

These changes are intended to reduce compliance complexity while maintaining the environmental effectiveness of CBAM. In particular, the de minimis threshold removes administrative obligations for very small importers while still keeping the vast majority of emissions within the scope of the mechanism.

Even with these simplifications, businesses importing CBAM-covered goods must still prepare for the definitive regime that began on 1 January 2026, including authorized declarant registration, emissions reporting, and certificate management ahead of the first financial settlement in 2027.

As the transitional phase ended, the Commission carried out its first review of CBAM in 2025 to evaluate how the system was functioning and whether its coverage should be expanded.

Following this review, the Commission published legislative proposals in December 2025 aimed at strengthening the mechanism and potentially expanding its scope. These proposals include extending CBAM to additional downstream products and introducing stronger anti-circumvention measures to prevent companies from restructuring supply chains to avoid the carbon price.

One likely direction for future expansion is the inclusion of additional product groups, such as organic chemicals and more downstream iron and steel products, as well as other sectors already regulated under the EU ETS.

There is also ongoing discussion about the scope of emissions covered by CBAM. At present, emissions coverage varies by sector. For example, cement and fertilizers include both direct and indirect emissions, while iron and steel, aluminum, and hydrogen currently focus primarily on direct emissions. The Commission is expected to assess whether indirect emissions should be more broadly incorporated in the future.

Here’s a simplified overview of the current roadmap:

| Phase | Timing | Application |

|---|---|---|

|

Definitive CBAM phase

|

From 2026 | The full CBAM regulatory framework is now in force. Importers must register as authorized CBAM declarants, monitor embedded emissions in their imports, and prepare for certificate management and annual declarations. |

|

First financial settlement

|

2027 | Importers will submit their first annual CBAM declaration and surrender certificates covering emissions embedded in goods imported during 2026. |

|

Possible scope expansion

|

2026–2030 | The European Commission may expand CBAM to additional downstream products and sectors already regulated under the EU ETS, such as organic chemicals and further processed iron and steel goods. |

|

Broader alignment with EU ETS

|

By 2030 (indicative) | Long-term objective to align CBAM coverage with EU ETS sectors and potentially expand the scope of emissions included in the mechanism. |

Although some expansion proposals have already been published, many of these changes still require approval through the EU legislative process and are not yet in force.

Businesses operating in sectors that could be brought into scope should therefore monitor regulatory developments closely and begin preparing for possible future compliance obligations. Companies that build strong emissions reporting and supply-chain transparency systems today will be better positioned to adapt as CBAM evolves in the coming years.

If you import CBAM-covered goods from outside the EU - such as steel, aluminum, cement, fertilizers, electricity, or hydrogen - you are now subject to the definitive CBAM regime, which began on 1 January 2026.

During the transitional phase (2023–2025), EU importers were required to report the embedded greenhouse gas emissions associated with their imports. Now that the definitive phase has begun, importers must prepare for the full CBAM compliance framework, including authorized declarant registration, annual emissions declarations, and certificate management.

The first financial settlement will take place in 2027, when importers submit their first annual CBAM declaration and surrender certificates covering emissions embedded in goods imported during 2026.

Here’s what importers need to know and start doing:

Since 1 January 2026, companies importing CBAM-covered goods into the EU must be registered as authorized CBAM declarants.

This authorization is granted by the National Competent Authority (NCA) in the EU member state where the importer is established.

To obtain authorization, importers typically need to:

One of the most challenging aspects of CBAM compliance is gathering accurate emissions data from non-EU manufacturers.

Importers should:

With the definitive phase now in force, importers must prepare for the full CBAM compliance framework.

This includes:

However, the first certificate surrender will take place in 2027, covering emissions embedded in goods imported during 2026.

CBAM compliance requires strong recordkeeping and data management. Importers should:

Given the complexity of CBAM and its evolving requirements, many businesses are choosing to work with third-party experts like Greenly to:

Choosing the right platform is key to smoothly navigating the EU’s Carbon Border Adjustment Mechanism (CBAM). The best CBAM-ready software helps businesses calculate embedded emissions, manage carbon pricing, and automate compliance reporting. Below we rank the 10 top solutions available - including Greenly as the leading option for end-to-end carbon management.

| Rank | Software | What it does | Best for | Available regions |

|---|---|---|---|---|

|

1

|

Greenly | Full carbon management platform covering CBAM reporting, carbon pricing, emissions tracking, and automated compliance workflows. | Importers, manufacturers, and exporters seeking a complete solution with expert guidance. | EU, UK, US |

|

2

|

EcoCarbon | CBAM-specific emissions tracking with integrated reporting templates for EU importers. | Small to medium-sized importers with simple product lines. | EU |

|

3

|

CarbonTrace | Advanced footprint calculations, scenario modeling for CBAM carbon pricing impacts. | Large manufacturers managing complex supply chains. | EU, North America |

|

4

|

EmisTrack | Automation for Scope 1–3 data collection and emissions verification aligned with CBAM requirements. | Multinational enterprises seeking centralized reporting. | Global |

|

5

|

CBAM SmartComply | Lightweight tool for exporters to quickly calculate embedded emissions and prepare declarations. | SMEs exporting to the EU. | EU, APAC |

|

6

|

ClimateBridge | Combines supplier engagement tools with CBAM-compliant footprint calculation. | Companies dependent on global supplier networks. | EU, Asia |

|

7

|

SustainPro | ESG-focused platform with CBAM modules for reporting and carbon pricing dashboards. | ESG teams in mid-to-large corporations. | EU, Americas |

|

8

|

CarbonLedger | Blockchain-based solution for traceable CBAM emissions data across supply chains. | Businesses needing verifiable data for regulators. | Global |

|

9

|

CBAM Assist | Entry-level calculator and reporting templates for quick CBAM compliance. | Small importers just starting CBAM reporting. | EU |

|

10

|

EnviroSoft | Broader sustainability platform offering optional CBAM reporting module. | Companies combining CBAM compliance with wider ESG tracking. | Global |

To comply with CBAM, companies importing covered goods into the EU need to calculate the embedded greenhouse gas emissions linked to their imports and make sure they are registered as authorized CBAM declarants where required. They will also need to submit annual CBAM declarations showing the volume of goods imported and the emissions associated with them, and purchase and surrender CBAM certificates to cover those emissions. Many businesses use CBAM-ready software to simplify the process by helping collect supplier data, calculate emissions, and generate the required declarations.

CBAM-ready software is designed to help companies manage their CBAM obligations more easily. These tools can calculate the embedded emissions of imported goods, gather emissions data from suppliers, and help prepare CBAM declarations using the EU’s methodology. Many platforms, like Greenly, also connect with broader ESG or sustainability reporting tools, making it easier to manage different compliance requirements in one place.

Yes. Many platforms, just like Greenly, now offer automation for things like emissions tracking, supplier data collection, data checks, and preparing CBAM declarations. This can save time and reduce manual work, especially for companies with complex supply chains. Some tools also help estimate potential CBAM certificate costs and track regulatory updates.

Most CBAM-ready tools are available across the EU and in major exporting regions such as the United States and Asia. Availability depends on the provider, including which markets they operate in and the languages and integrations they support.

The right CBAM software will depend on your company’s size and how complex your supply chain is. Larger companies with many suppliers may benefit from more advanced platforms that handle detailed emissions calculations and supplier engagement. Smaller importers might only need a simpler tool focused on emissions tracking and CBAM declarations. In general, it’s useful to look for software that can calculate embedded emissions, collect supplier data, support CBAM declarations, and help estimate carbon pricing exposure.

While CBAM is an EU regulation, US companies exporting to Europe will still feel its effects. Goods produced in the US and exported to the EU can fall within the scope of CBAM if they belong to one of the covered sectors, such as steel, aluminium, cement, fertilisers, electricity, or hydrogen.

Under CBAM, the legal reporting and certificate obligations fall on the EU importer, not the non-EU exporter. The importer must report the greenhouse gas emissions embedded in the goods and, under the definitive regime, surrender CBAM certificates covering those emissions.

However, US exporters still play a key role because EU importers rely on them to provide accurate emissions data for the products they sell.

For US businesses, this means:

As the EU begins pricing the carbon embedded in imported goods, companies supplying the European market may face growing pressure to reduce emissions, improve transparency, and demonstrate lower-carbon production methods.

CBAM reporting for importers of goods manufactured outside the EU doesn’t have to be a manual, spreadsheet-heavy nightmare.

Greenly’s purpose-built platform streamlines the entire process for both EU importers and their international suppliers.

Here’s how we help:

| How Greenly supports CBAM compliance | What it means |

|---|---|

|

Emissions tracking

|

Greenly’s platform supports data collection across both direct and indirect emissions, helping you meet EU methodology requirements and avoid reporting gaps. |

|

Streamline supplier data collection

|

Use tailored CBAM questionnaires, automated follow-ups, and supplier-specific dashboards to collect accurate emissions data – no spreadsheets required. |

|

Track evolving supply chains

|

As new products or suppliers are added, Greenly automatically triggers new data requests, keeping your reporting up to date without extra admin. |

|

Centralized supplier collaboration

|

Give your suppliers access to their own dedicated portal where they can upload data, access guidance, and contribute directly to your reports. |

|

Improve accuracy, reduce risk

|

Built-in quality checks and real-time insights help you spot issues early, reduce reporting errors, and stay ahead of rising carbon allowance costs. |

|

Automate quarterly reporting

|

Generate compliant XML reports in minutes, ready for direct upload to the EU portal. Our platform detects CBAM goods, flags missing data, and handles formatting automatically. |

Whether you’re an EU declarant or an international supplier, Greenly’s all-in-one CBAM solution is designed to save time, lower costs, and help you reduce emissions while staying compliant.

Share this article

What is decarbonization, and why is it urgent? Learn practical steps companies can take to support the global move toward net zero emissions.

In this article, we’ll break down what IROs are, how to identify and assess them, and what CSRD requires in terms of disclosure.