Greenlyhttps://www.greenly.earth/https://images.prismic.io/greenly/43d30a11-8d8a-4079-b197-b988548fad45_Logo+Greenly+x3.pngGreenly, la plateforme tout-en-un dédiée à toutes les entreprises désireuses de mesurer, piloter et réduire leurs émissions de CO2.Greenlyhttps://www.greenly.earth/Greenly, la plateforme tout-en-un dédiée à toutes les entreprises désireuses de mesurer, piloter et réduire leurs émissions de CO2.Descending4

Home

1

Blog

2

Category

3

EU ETS: what you need to know about the EU carbon market

In this article, we'll explore the EU Emissions Trading System (EU ETS), a European initiative for reducing greenhouse gases through a cap-and-trade scheme.

The EU Emission Trading System (EU ETS) is a key component of Europe's environmental strategy, but what exactly is it and how does it function?

This article aims to demystify the EU ETS, offering an overview of its structure, operation, and impact. We'll delve into how this system has become a crucial tool in the EU's efforts to reduce greenhouse gas emissions, discuss its economic implications, and examine the challenges it faces as it undergoes a major 2026 legislative review to align with the EU's 2040 climate targets.

In this article, we'll explore:

What the EU ETS is

How the system functions

The 2024–2026 expansion

The new "ETS2" system

The start of CBAM payments

What is the EU ETS?

The European Union Emission Trading System, commonly known as the EU ETS, represents a major step in Europe's commitment to fighting climate change. Established in 2005, it is the world's first and largest international trading system for carbon dioxide emissions, a pioneering model for cap-and-trade schemes globally.

At its core, the EU ETS operates on a straightforward principle: setting a cap on the total amount of certain greenhouse gases that can be emitted by installations covered by the system. The cap is reduced over time, helping the EU to progress towards its emissions reduction target. Within this system, companies receive or buy emission allowances, which they can trade with one another as needed. Each allowance equals one tonne of CO2 equivalent (CO2e), covering carbon dioxide, methane, and nitrous oxide in specific sectors.

The EU ETS covers over 10,000 power stations and industrial plants across EU member states, Iceland, Norway, and Liechtenstein, as well as airlines operating between these countries. Since 2024, the system has included maritime transport, with 2026 marking the first year shipping companies must surrender allowances for 100% of their reported emissions. It accounts for approximately 45% of the EU's greenhouse gas emissions, and as of 2024, the system successfully halved emissions in covered sectors compared to 2005 levels.

The evolution of the EU ETS

The EU ETS is not static; it has evolved through four distinct phases to become more stringent and wide-reaching.

2005–2007

Phase 1 — The Pilot Phase

A “learning by doing” period. The ETS initially covered only CO₂ emissions from power generators and energy-intensive industries. Most allowances were allocated for free.

2008–2012

Phase 2 — Expansion

The system widened in scope as Iceland, Norway, and Liechtenstein joined. Aviation was added in 2012, and the ETS began allowing the limited use of international carbon offsets.

2013–2020

Phase 3 — Centralisation

A single EU-wide cap replaced national caps. Auctioning became the default allocation method, marking a shift away from widespread free allocation.

2021–2030

Phase 4 — The “Fit for 55” Era

The annual cap reduction accelerated to 4.3%. This phase also brings major extensions, including maritime transport in 2024 and the launch of the CBAM in 2026, aimed at limiting carbon leakage.

2031–2050

Post-2030 — Path to Net Zero

The ETS is expected to evolve further as the EU aligns it with its longer-term climate objectives.

A major legislative review is currently underway, with a review scheduled for July 2026, to support alignment with the EU’s 2040 target.

Why this evolution matters in 2026

The EU ETS has reached a pivotal turning point in Phase 4. As of early 2026, the system has moved beyond simply taxing pollution to actively driving a total industrial overhaul. This year marks the start of the permanent phase for the Carbon Border Adjustment Mechanism (CBAM), ensuring that international importers face the same carbon costs as European manufacturers. By effectively equalizing the playing field, the EU is now exporting its carbon-pricing model to the global stage.

At the same time, the market is preparing for the July 2026 Review. This landmark legislative update is expected to shape the ETS framework for the next decade, with a high-level focus on integrating Carbon Dioxide Removals (CDR). This shift would allow companies to meet climate targets not only by reducing their output but by supporting technologies that actively remove and store carbon from the atmosphere.

Close

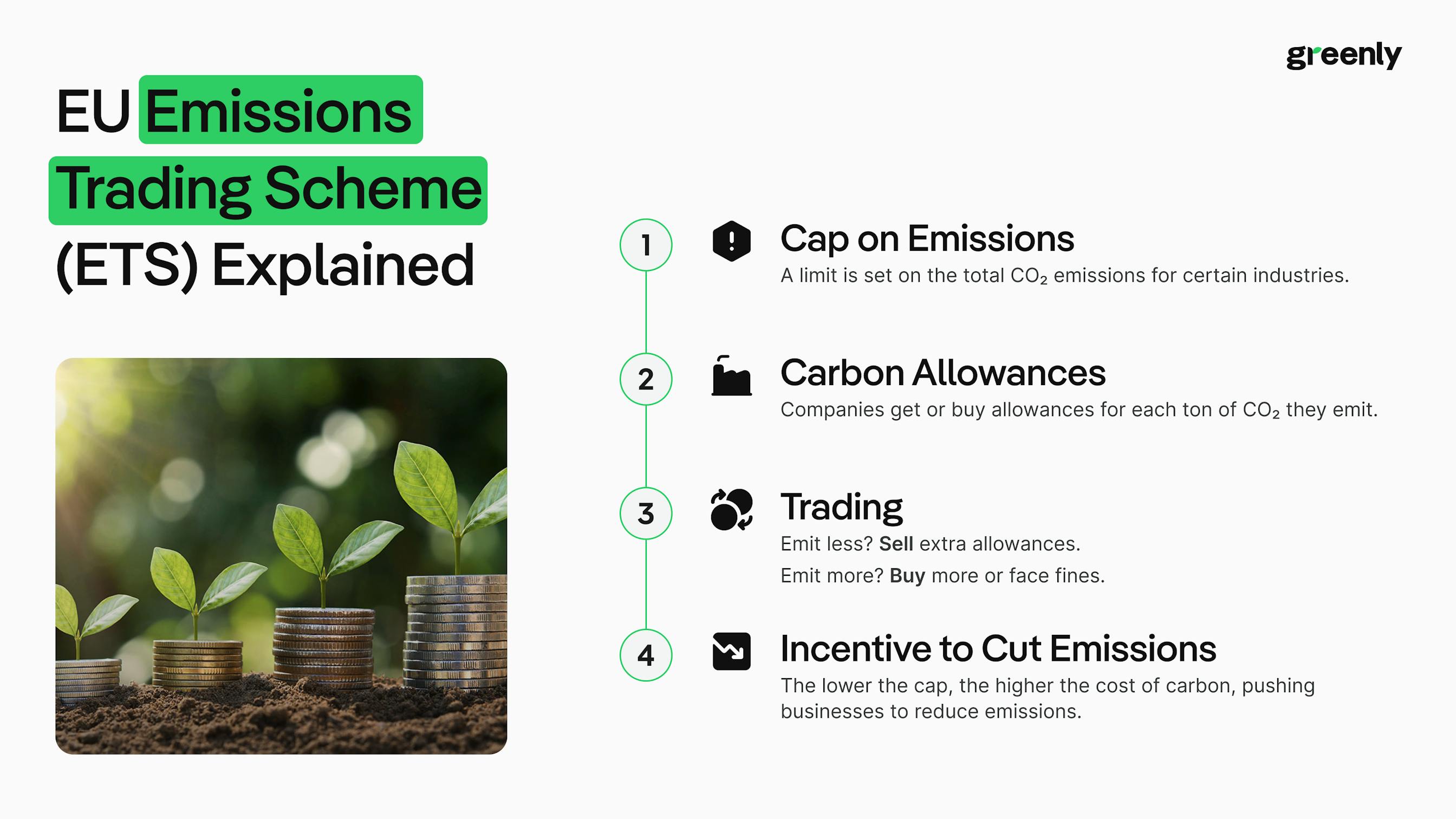

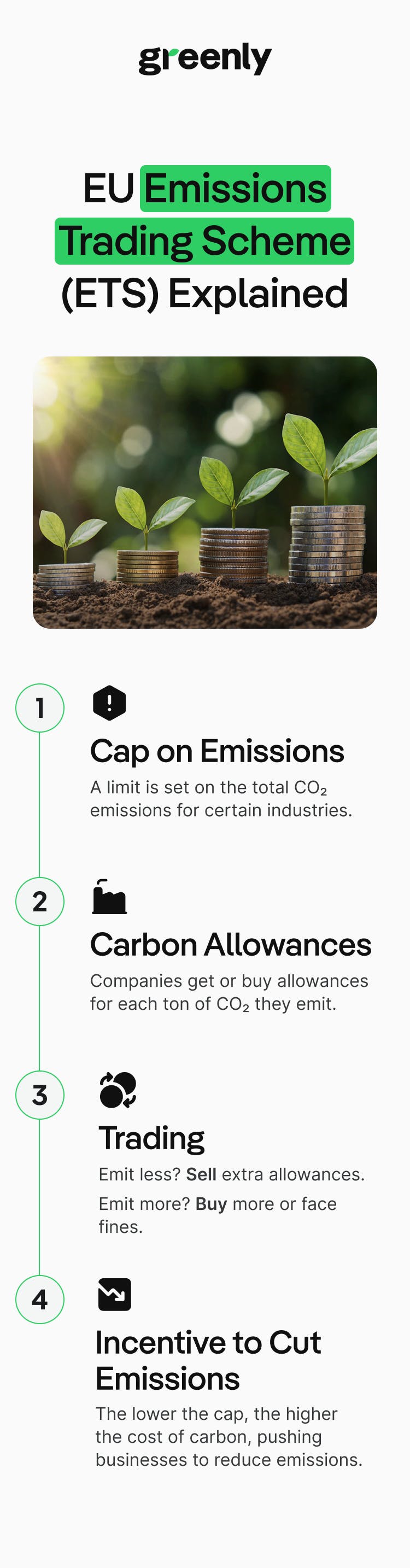

How does the EU ETS work?

The system operates on a 'cap-and-trade' principle, a method that combines regulatory limits with market-based incentives. Let's take a closer look at how this functions:

Setting the cap:

The EU ETS sets an upper limit or ‘cap' on the total amount of certain greenhouse gases that can be emitted by factories, power plants, and other installations that fall under the scope of the system. This cap is reduced annually - currently at a rate of 4.3% per year - to align with the EU's target of a 62% reduction in ETS-covered sectors by 2030.

Allocation of EU allowances:

Within this cap, companies receive or buy emission allowances, which are essentially permits to emit a certain amount of greenhouse gases. One allowance grants the holder the right to emit one tonne of CO2 equivalent (CO2e). While around 57% of the cap is currently auctioned, the remaining allowances are provided for free to industries at high risk of carbon leakage (relocating production outside the EU).

However, as of January 2026, these free allowances have begun a gradual phase-out for sectors now covered by the Carbon Border Adjustment Mechanism (CBAM).

Trading in the European carbon market:

The 'trade' aspect allows for flexibility; firms that reduce their emissions can sell their excess allowances to those who need more. This trading occurs at market prices, which fluctuate based on supply, demand, and the volume of permits held in the Market Stability Reserve (MSR).

Verified emissions and compliance

The annual compliance cycle is central to the system:

📊

Monitoring & Reporting

Operators must track their emissions continuously throughout the calendar year.

✔️

Verification

By March 31 of the following year, emissions must be verified by an accredited third party.

🧾

Surrendering Allowances

Operators must surrender the corresponding number of allowances annually.

Deadline: September 30 (moved from April 30 in 2024)

Compliance and penalties

Missing the September 30th deadline is a costly mistake. For every tonne of carbon not covered by an allowance, companies face an automatic fine. While the base rate is set at €100, this is indexed to inflation and has risen every year; in 2026, the effective penalty is approximately €118 per tonne.

Paying this fine does not cancel out the debt. The company must still surrender the missing allowances the following year, and their name is added to a public name and shame list released by the European Commission.

“The EU ETS is not just about limiting emissions; it's also about driving innovation. By putting a price on carbon, it encourages investment in greener technologies and practices. The revenue generated from the auctioning of allowances is often reinvested in climate and energy projects, further amplifying the system's positive impact.”

Close

EU ETS expanding scope

The EU ETS has undergone a massive transformation, shifting from a system focused on heavy industry to a comprehensive framework covering around75% of the Union's total greenhouse gas emissions.

EU ETS: 2026 changes by sector

🏠

1. The New ETS2 for Buildings and Transport

Status: Reporting active; Trading officially postponed to 2028.

Following the price-assessment review in mid-2026, the EU has officially activated the delay clause, pushing the start of the ETS2 trading system from 2027 to 2028. This was done to ensure a smoother transition amidst fluctuating energy markets.

The 2026 Milestone

While trading starts later, fuel distributors are currently in their first mandatory verification cycle. Any 2025 emissions data being reported now (Spring 2026) must be verified by an accredited third party.

Social Climate Fund (SCF)

The SCF officially launched in March 2026. It is now actively funding projects in Member States to help vulnerable households invest in heat pumps and electric vehicles before the 2028 carbon price kicks in.

✈️

2. Aviation: The End of Free Permits

Status: Full Auctioning (100%) as of 2026.

The era of free "grandfathered" permits for airlines has ended. As of January 1, 2026, all airlines operating within the EEA must purchase 100% of their allowances at auction.

The July 2026 Review

All eyes are on the upcoming July 1, 2026 report. The Commission is currently assessing the global CORSIA scheme; if it's deemed insufficient, the EU ETS is legally set to expand to cover all departing international flights starting in 2027.

🚢

3. Maritime: Full Implementation

Status: 100% surrender requirements active.

The maritime phase-in is complete. Shipping companies must now surrender allowances for 100% of their verified emissions for intra-EU voyages.

Beyond CO2

Starting this year (2026), the scope has expanded to include Methane (CH4) and Nitrous Oxide (N2O). This is a major technical hurdle for LNG-vessel operators, who must now account for "methane slip" in their compliance.

CO2CH4N2O

🗑️

4. New: Municipal Waste Incineration

Status: Monitoring active; Inclusion decision expected July 2026.

Since 2024, large municipal waste incineration plants (over 20MW) have been required to monitor and report their emissions. As part of the July 2026 legislative review, the Commission will decide whether to fully integrate these plants into the ETS with an obligation to surrender permits starting in 2028.

ETS2 2025 emissions data enters mandatory verification cycle.

March 2026

Social Climate Fund officially launches.

July 1, 2026

Major review point for aviation and waste incineration decisions.

2027

Potential international flight scope expansion, subject to review outcome.

2028

ETS2 trading start; possible waste incineration surrender obligation.

CBAM: Extending the EU ETS to the global market

The Carbon Border Adjustment Mechanism (CBAM) is the EU's landmark tool for equalizing the cost of carbon between domestic products and imports. As of January 1, 2026, CBAM officially transitioned from a reporting-only phase into its definitive regime, meaning that financial liability for importers is now a reality.

The connection: CBAM and EU ETS free allocation

The most important thing for companies to understand in 2026 is that CBAM and the EU ETS are designed to work as a single, unified price floor. To comply with international trade rules (WTO), the EU cannot charge importers for carbon while giving its own domestic industries a free pass.

This is why, as of January 1, 2026, the EU has launched a mirrored "Symmetry" phase:

🏭

For Domestic Manufacturers

The "Free Allocation" of permits they used to receive under the EU ETS is now being phased out. In 2026, these free permits have been cut by an initial 2.5%, and will continue to drop every year until they reach zero in 2034.

2.5% cut in 2026 · zero by 2034

📦

For Importers

To match that loss of domestic protection, the CBAM financial obligation has officially begun. Importers must now purchase CBAM certificates at a price that mirrors the actual cost of carbon on the EU market.

CBAM certificates now required

How the price is set in 2026

You aren't dealing with a static tax; you are dealing with a live market price.

📊

The Benchmark

The price of a CBAM certificate is tied directly to the EU ETS allowance (EUA) price.

Linked to EUA carbon price

📅

The 2026 Calculation

For this first year of the definitive phase, the Commission is publishing quarterly average prices. The first official price for Q1 2026 has been set at €75.36 per certificate.

Q1 2026: €75.36

⚖️

The 50% Rule

To ensure compliance, authorized declarants must ensure their account holds certificates covering at least 50% of the embedded emissions of their imports by the end of each quarter.

Minimum 50% coverage each quarter

Why this is a game-changer for strategy

In 2026, carbon has officially moved from the Sustainability Report to the Balance Sheet.

🔍

Supply Chain Audits

Because default values (estimated emissions) are now significantly more expensive than actual verified data, companies are currently racing to audit their international suppliers to prove their goods are lower-carbon.

Verified data vs default values

📉

Hedging Costs

Since the price of importing steel or aluminum now fluctuates with the EU ETS market, procurement teams are having to learn the mechanics of carbon trading to hedge against price spikes.

Exposure to carbon price volatility

🧾

The July 2026 Scope Review

The Commission is currently reviewing whether to expand CBAM to include indirect emissions (the electricity used in production) and downstream products (like screws, bolts, and car parts) as early as 2027.

Potential expansion in 2027

How does the EU ETS impact US companies?

The US does not have a national carbon market like the EU or UK. However, as of 2026, the EU ETS has become a "de facto" regulator for American exporters. Any US company selling carbon-intensive goods into Europe now faces a choice: prove your products are "cleaner" than the global average or pay a premium at the border.

The 'clean data' defense

Since there is no US federal carbon price to "offset" the EU's fees, American firms have to compete on efficiency. The goal for US manufacturers right now is to prove they are cleaner than the global average to lower their "carbon bill" at the European border.

📜

The PROVE IT Act

Signed into law in January 2026, this act directed the US Department of Energy to officially verify how much cleaner American manufacturing is compared to other countries.

Signed into law in January 2026

🛡️

The Advantage

US companies are using this government-verified data to fight the EU’s default values. If you don’t have your own verified data, the EU applies a worst-case scenario carbon estimate to your products, making them much more expensive for European buyers.

Verified data helps avoid default values

EU CBAM: The new cost for US exporters

For American firms, the reporting-only days are over. Since January 1, 2026, the financial obligations are live.

⚠️

The 10% Surcharge

If a US exporter fails to provide verified data, the EU applies the high default value plus a 10% penalty markup. This makes unverified US steel significantly less competitive in the European market.

Penalty + default value applied

⏱️

The Auditor Bottleneck

US firms must now hire EU-accredited auditors to sign off on their emissions data. Because everyone is trying to do this at once, wait times have skyrocketed, making it a gating issue for reaching European customers.

Access to EU market depends on verification

📊

July 2026 Review

The EU is currently deciding whether to start charging for the electricity used in US factories (indirect emissions). For plants in US states that still rely heavily on coal, this could suddenly spike the cost of exporting to Europe.

Potential cost increase from indirect emissions

The US response: The Clean Competition Act

The US is currently finalizing its own answer to the EU. The Clean Competition Act, reintroduced in late 2025 and gaining steam in early 2026, would create a mirrored American border fee.

🏆

Reward for the Cleanest

Unlike the EU's blanket system, the proposed US law only charges a fee if a product's emissions are worse than the US industry average.

Only above-average emissions are penalised

🛡️

The Strategy

This would protect clean American factories by taxing 'dirty' imports from countries with lower environmental standards.

Targets high-emission imports

Practical steps for businesses dealing with the EU ETS

The EU ETS and CBAM have moved from policy discussions to line-item expenses. To avoid penalties and manage rising carbon costs, companies should prioritize the following actions this year:

🏭

For Industrial & Power Installations

Free Allocation Audit: Review your energy audit recommendations. Under current rules, receiving your full share of free permits is tied to performance; failing to implement efficiency measures can lead to an automatic 20% reduction in your allocation.

The Compliance Calendar: Ensure your internal reporting cycle aligns with the September 30th surrender deadline. This is a permanent shift from the old April deadline; missing it triggers significant penalties and public disclosure.

Baseline Reporting: Verify that your multi-year baseline data is accurate and submitted. This data locks in your standing for the current trading period.

🚢

For Shipping & Maritime Operators

Full Emissions Accounting: With the phase-in period concluded, ensure your budgets now account for 100% of emissions on intra-EU voyages.

Broadening the Scope: Compliance reports must now include Methane (CH4) and Nitrous Oxide (N2O), not just CO2. This requires more granular data from engine monitoring systems.

Contractual Clarity: Review charter party agreements (using industry standards like BIMCO clauses) to ensure clear legal responsibility for carbon costs between owners and charterers.

📦

For Importers and Supply Chain Managers

Authorised Status: Confirm your company is registered as an Authorised CBAM Declarant. This is now a prerequisite for importing covered goods like steel, aluminum, and chemicals.

Quarterly Compliance: Maintain a true-up process. You are required to hold certificates covering at least half of your year-to-date imported emissions by the end of each quarter to ensure liquidity.

Verified Data over Defaults: Default values for carbon are designed to be expensive. Transition your suppliers from estimates to verified emissions data to reduce the number of certificates you need to purchase.

⛽

For Fuel Distributors (ETS2)

The Reporting Cycle: While the trading system for buildings and transport has a delayed start for payments, the monitoring and verification cycle is active. Secure your third-party auditors early to avoid the year-end rush.

Funding the Transition: Investigate eligibility for the Social Climate Fund. These grants are designed to support the switch to electric fleets and energy-efficient heating before carbon pricing impacts fuel costs.

EU ETS challenges and opportunities

The EU ETS has reached a stage where it is no longer just a pollution tax - it has become a massive economic engine. While the transition creates real pressure, it is also unlocking record levels of investment.

1. High Carbon Prices: A Double-Edged Sword

The Pressure

Carbon prices in 2026 have stabilized at a high level (often between €70 and €85 per tonne). For companies still relying on old, fossil-fuel-heavy processes, this creates significant financial strain on their quarterly balance sheets.

The Opportunity

This same price signal has made green projects financially viable for the first time. In early 2026, the EU announced that over 50 major industrial projects have reached their final investment decision because fossil fuels are now the more expensive option.

2. Competitive Symmetry with CBAM

The Pressure

As free permits are phased out, EU manufacturers face higher costs than some of their global competitors.

The Opportunity

CBAM levels the playing field. Importers of high-carbon goods must now pay the same carbon entry fee, encouraging global suppliers to reduce emissions.

3. Turning Tax into Investment

Carbon costs

→

EU ETS revenue

→

Clean tech investment

The revenue from the EU ETS is recycled directly back into industry. In March 2026, €2.7 billion was unlocked for 54 clean-tech projects across 17 countries via the Innovation Fund. At the same time, the Social Climate Fund is supporting businesses and households in transitioning to cleaner energy solutions.

4. Innovation in Hard-to-Abate Sectors

The 2026 review is exploring how to support sectors that cannot reach zero emissions through efficiency alone. A key focus is Carbon Dioxide Removals (CDR), potentially allowing companies to earn or trade credits for removing carbon from the atmosphere, creating a new industrial market.

The future of the EU ETS

The EU ETS has evolved from a simple pilot program into the central pillar of Europe's industrial strategy. As we move further into Phase 4, the focus is shifting toward long-term stability and the next generation of climate targets.

The 2040 milestone

In March 2026, the EU reached a major landmark by officially amending the European Climate Law to include a 90% net emission reduction target for 2040. This target provides a goal for the EU ETS, ensuring that the annual reduction in allowances (the cap squeeze) will continue until the market effectively reaches zero emissions.

The July 2026 review

The upcoming July 2026 legislative review is set to be the most significant update in years. The European Commission is currently evaluating several key expansions that will shape the market post-2030:

🌱

Negative Emissions

Exploring how to integrate "Carbon Removals" into the trading system, allowing companies to meet their obligations by funding technologies that remove CO2 from the atmosphere.

Carbon removals integration

🗑️

Waste & Small Installations

Final decisions are expected on whether to fully include municipal waste incineration and smaller combustion plants (below 20MW) into the system.

Inclusion decision pending

✈️

International Aviation

A review of the global CORSIA scheme will determine if the EU ETS will expand to cover all departing international flights starting in 2027.

Potential expansion in 2027

A global benchmark

By 2030, nearly all goods covered by the EU ETS will also be under the umbrella of CBAM. This integration signifies the EU's move toward a globally aligned climate policy, where the 'European price' for carbon becomes a benchmark for international trade.

“The journey ahead is about more than just hitting targets; it’s about transforming Europe into a climate-neutral industrial powerhouse. For businesses, the message is clear: the carbon market is here to stay, and those who lead in decarbonization today will be the most competitive players in the 2040 economy.”

EU ETS FAQs:

What is the penalty for non-compliance?

The standard fine remains €100 per tonne of excess emissions, but it is adjusted annually for inflation. For the 2026 compliance cycle, the effective penalty has risen to approximately €118 per tonne. Importantly, paying the fine does not exempt you from surrendering the missing allowances; you must still provide them in the next reporting cycle, and your company name will be published on the EU’s non-compliance list.

Is the "ETS2" (Buildings and Transport) still launching in 2027?

No. In late 2025, the EU officially triggered the delay clause due to high energy prices. The definitive phase (where you must pay for allowances) is now set to begin on January 1, 2028. However, the reporting and verification obligations are already active - fuel distributors must monitor and verify their 2025 data this spring.

Does the EU ETS now include Methane (CH4) and Nitrous Oxide (N2O)?

Yes, but currently only for the Maritime sector. As of January 1, 2026, shipping operators must include these gases in their verified reports. For aviation and stationary industrial installations, the system still primarily focuses on CO2, though the July 2026 Review is expected to propose expanding this to other greenhouse gases for all sectors by 2028.

What is the Market Stability Reserve (MSR) update for 2026?

The Commission has proposed a change to the MSR to prevent the automatic cancellation of allowances. Instead of being deleted, excess allowances will be held in the reserve to act as a buffer. This is intended to prevent extreme price spikes (volatility) by ensuring the EU can release more permits if the market becomes too tight.

Can companies use 'Carbon Removal' credits to meet our 2026 targets?

Not yet. Currently, you cannot use credits from Direct Air Capture (DAC) or other removal technologies to meet your ETS obligations. However, this is one of the biggest topics of the July 2026 Review. The EU is designing a framework to potentially integrate 'Certified Carbon Removals' into the market after 2030.

When is the next major 'Free Allocation' update?

We are currently in the middle of the 2026–2030 allocation period. If your installation’s production levels have changed by more than 15% (up or down) compared to your reported baseline, you must notify your national authority immediately, as your free allowance volume will be adjusted annually to reflect your actual activity.

Close

How Greenly can help your company

Streamlined ESG Data Management & Compliance

Greenly streamlines the complex process of ESG data collection, consolidation, and management all in 1 platform.