Greenlyhttps://www.greenly.earth/https://images.prismic.io/greenly/43d30a11-8d8a-4079-b197-b988548fad45_Logo+Greenly+x3.pngGreenly, la plateforme tout-en-un dédiée à toutes les entreprises désireuses de mesurer, piloter et réduire leurs émissions de CO2.Greenlyhttps://www.greenly.earth/Greenly, la plateforme tout-en-un dédiée à toutes les entreprises désireuses de mesurer, piloter et réduire leurs émissions de CO2.Descending4

EFRAG’s voluntary SME reporting standard explained: Basic and Comprehensive modules, key disclosures, the Omnibus I value chain cap, and how to get started.

For many small and medium-sized businesses, sustainability reporting has become a practical reality: banks ask for ESG data before approving financing, large clients request it as a condition of doing business. But until recently, there was no single standardised way to respond.

The VSME standard — the Voluntary Sustainability Reporting Standard for non-listed SMEs — is a free, modular ESG reporting framework developed by EFRAG at the request of the European Commission. Formally adopted via Commission Recommendation (EU) 2025/1710 on 30 July 2025, it gives non-listed SMEs a single, proportionate framework for responding to sustainability data requests from banks, investors, and large corporate clients.

In this article, we break down how the VSME standard works, what the Omnibus I value chain cap means for SMEs, and how UK businesses can get started with VSME reporting.

In this article, we'll explore:

What the VSME standard is and why the European Commission introduced it

How the Basic and Comprehensive modules work, and which one your business needs

What the Omnibus I value chain cap means for SMEs in practice

How the VSME standard compares to GRI and what it does not require

How UK businesses can start putting the VSME standard into practice

What is the VSME standard?

The Voluntary Sustainability Reporting Standard for non-listed SMEs (VSME) is a free, voluntary ESG reporting framework developed by EFRAG for non-listed micro, small, and medium-sized enterprises. It covers environmental, social, and governance topics across two reporting modules — Basic and Comprehensive — with no materiality assessment required.

The European Financial Reporting Advisory Group (EFRAG) developed the VSME at the request of the European Commission, responding to the growing demand for ESG data from SMEs. While larger companies and financial institutions already follow strict sustainability reporting requirements under the Corporate Sustainability Reporting Directive (CSRD), non-listed SMEs are not legally required to disclose ESG information. However, in practice, many SMEs are expected to provide sustainability data to meet the demands of their clients, investors, and banks.

The VSME aims to simplify this process by offering a structured but flexible reporting framework. Instead of SMEs having to complete multiple, uncoordinated ESG questionnaires, the VSME provides a single standard that stakeholders can use to assess sustainability performance.

The VSME standard was originally developed and formally adopted for non-listed micro, small, and medium-sized enterprises with fewer than 250 employees. Following the Omnibus I Directive (EU) 2026/470, which entered into force in March 2026, companies with up to 1,000 employees that fall outside the mandatory CSRD scope can also use the VSME framework to respond to ESG data requests from banks, investors, and large corporate clients. A future Delegated Act, currently in adoption proceedings and expected in July 2026, will give the VSME standard formal legal standing for this broader group, though its final content may differ slightly from the Commission Recommendation adopted on 30 July 2025.

How the VSME differs from the CSRD

While the CSRD mandates ESG reporting for large companies and listed SMEs, the VSME is entirely voluntary. It is also:

🧩

Simpler and more proportionate:

The VSME is tailored to the needs and capabilities of small and medium-sized businesses, stripping away unnecessary complexity.

🔄

Flexible:

Companies can choose between a Basic and a Comprehensive reporting module depending on their needs.

In short, the VSME is not a regulatory requirement, but it is a strategic opportunity. For SMEs looking to stay competitive, attract financing, and future-proof their business, adopting the VSME could be a smart move.

Close

Why was the VSME introduced?

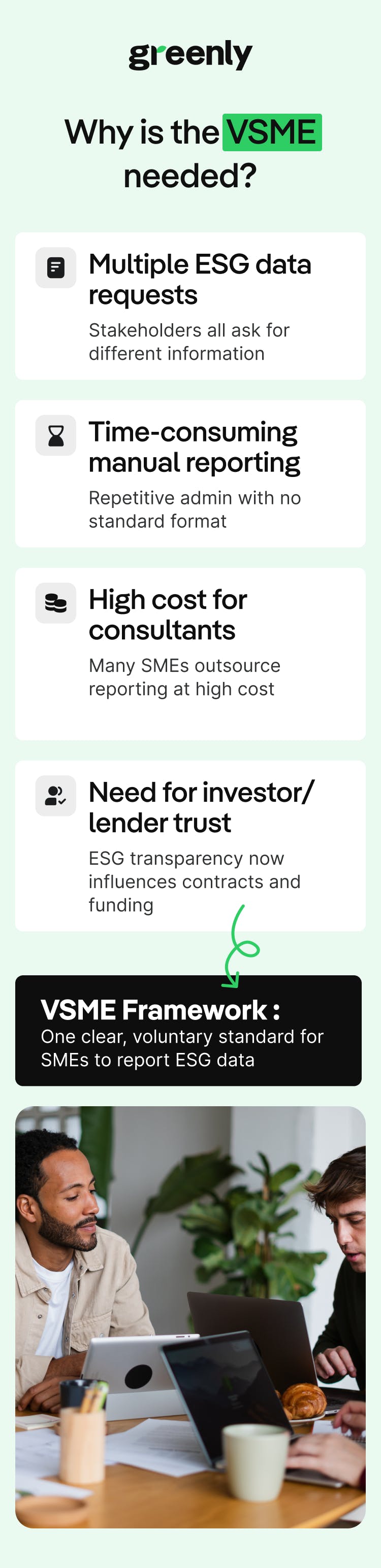

For many companies, sustainability reporting is becoming an unavoidable part of doing business. Whether applying for loans, securing investment, or maintaining supplier contracts with larger companies, SMEs are increasingly expected to provide environmental, social, and governance data.

The problem? There's no single, standardised way for SMEs to report on sustainability. Instead, many businesses receive multiple ESG data requests from banks, investors, and corporate clients, each with different formats, questions, and expectations.

This creates three major challenges for micro, small, and medium companies:

⏳

Time and resource burden

Small and medium-sized businesses often lack the expertise and staff to produce sustainability reports, let alone customise them for different stakeholders.

💰

High costs

Gathering sustainability information and data, responding to requests, and potentially hiring consultants all come with a price tag.

🚪

Risk of lost opportunities

Without an easy way to provide ESG information, businesses may struggle to access green financing, secure contracts with larger companies, or attract sustainability-focused investors.

When developing the VSME standard, EFRAG ran a public consultation that received responses from 311 organisations and 22 written submissions, including banks, investors, large companies, and SMEs themselves. The feedback confirmed that the fragmented ESG questionnaire landscape was creating a significant burden on smaller businesses, and directly shaped the design of both reporting modules. (European Commission Q&A, 30 July 2025)

The European Commission's response: The SME Relief Package

Recognising these challenges, the European Commission included the VSME as part of its SME Relief Package, published in September 2023. The goal? To provide a simple, standardised sustainability reporting framework for non-listed SMEs.

The European Financial Reporting Advisory Group (EFRAG) was then tasked with developing the VSME standard, which was delivered to the Commission on December 17, 2024.

Latest update: Commission Recommendation adopted 30 July 2025

On 30 July 2025, the European Commission formally adopted the VSME as Commission Recommendation (EU) 2025/1710, making it the official voluntary ESG reporting standard for non-listed SMEs across the EU. The Recommendation has also been published in all EU languages, making the VSME framework accessible to businesses across Europe.

What the VSME aims to solve

By introducing a voluntary but standardised ESG reporting tool, the VSME is expected to:

📉

Reduce the reporting burden

One framework instead of multiple ad-hoc data requests.

💼

Attract investors and lenders

A clear ESG report can improve financing opportunities for SMEs.

🌱

Integrate sustainability

Simplified reporting encourages more businesses to track their sustainability efforts.

Close

Structure of the VSME: Two reporting modules

The Voluntary Sustainability Reporting Standard for SMEs (VSME) follows a modular structure, allowing businesses to choose between:

1

Basic Module:

Covers 11 key disclosures and serves as the minimum reporting level for all SMEs.

2

Comprehensive Module:

An optional extension with 9 additional disclosures for SMEs that want to report more detailed ESG information.

This approach ensures that even the smallest businesses can engage in sustainability reporting without being overwhelmed by unnecessary complexity.

1. The Basic Module: Essential ESG disclosures

The Basic Module is the starting point for all companies adopting the VSME. It includes 11 key disclosures across environmental, social, and governance (ESG) topics:

Category

Disclosure

Description

General Information

1. Basis for preparation

States the reporting framework chosen (Basic or Comprehensive Module) and general company details (legal form, turnover, employee count, etc.).

2. Sustainability practices & plans

Describes the SME's sustainability-related policies and any planned improvements.

Environmental Metrics

3. Energy & GHG emissions

Reports total energy consumption and direct (Scope 1) and indirect (Scope 2) GHG emissions.

4. Pollution

Discloses pollutants emitted to the environment if required by regulations or voluntary reporting systems.

5. Biodiversity

Reports whether business sites are located in or near biodiversity-sensitive areas.

6. Water

Reports water consumption and withdrawals, especially in water-stressed regions.

7. Resource use & circular economy

Reports on waste generation, recycling efforts, and circular economy initiatives.

Social Metrics

8. Workforce – General

Provides employee data, including full-time/part-time breakdown and gender distribution.

9. Workforce – Health & safety

Reports workplace incidents, including work-related injuries and fatalities.

10. Workforce – Remuneration & rights

Discloses minimum wage compliance, pay gap, union representation, and employee training hours.

Governance Metrics

11. Anti-corruption

Reports any corruption-related convictions and financial penalties, offering insight into the company’s approach to corporate governance and ethical conduct.

The Basic Module provides a streamlined, practical approach to ESG reporting while ensuring that companies can easily share relevant sustainability data with investors, lenders, and business partners.

2. The Comprehensive Module: Additional ESG disclosures

For companies that want to enhance their sustainability reporting, the Comprehensive Module adds 9 more disclosures to the Basic Module. These disclosures are particularly useful for businesses seeking green financing, partnerships with sustainability-driven corporations, or alignment with investor expectations.

Category

Disclosure

Description

General Information

1. Strategy: Business model & sustainability

SMEs must disclose their business model and any key sustainability initiatives that are part of their strategy.

2. Policies & future transition initiatives

Businesses must describe their sustainability-related policies and planned sustainability improvements.

Environmental Metrics

3. GHG reduction targets & climate transition

SMEs must disclose any specific targets for reducing greenhouse gas emissions and their strategy for transitioning towards a low-carbon business model.

4. Climate risks

SMEs must assess and report their exposure to climate-related risks, including physical risks (e.g., extreme weather events) and transition risks (e.g., regulatory changes).

Social Metrics

5. Workforce – Additional characteristics

Further workforce details beyond the Basic Module, including employment type and breakdowns by contract type and region.

6. Human rights policies & processes

Disclosure of company policies related to human rights, including labor rights protections, non-discrimination measures, and grievance mechanisms.

7. Severe human rights incidents

SMEs must report any confirmed incidents of severe human rights violations, such as forced labor, child labor, or other serious breaches.

Governance Metrics

8. Revenues & EU benchmark exclusions

SMEs must disclose revenue from sectors such as fossil fuels, tobacco, or other industries considered high-impact. They must also report whether they are excluded from EU sustainability reference benchmarks.

9. Gender diversity in governance

SMEs must disclose the gender composition of their governance bodies, including senior leadership and board-level representation.

3. Choosing the right module: What companies need to consider

If an SME wants to…

Recommended Module

Meet basic ESG expectations

Basic Module

Simplify sustainability reporting for clients and lenders

Basic Module

Secure investment from sustainability-focused investors

Comprehensive Module (in addition to the Basic Module)

Position itself as a sustainability leader

Comprehensive Module (in addition to the Basic Module)

Important: The Comprehensive Module cannot be used on its own — a business must first complete the Basic Module before adding the additional disclosures.

This modular approach ensures that companies can scale their sustainability reporting efforts depending on their business needs and stakeholder expectations.

How the VSME connects to ESRS and other financial regulations

The VSME was designed to be compatible with the European Sustainability Reporting Standards (ESRS), meaning data collected for the VSME feeds directly into the value chain disclosures that large CSRD-reporting companies need from their suppliers.

The Basic Module covers the core ESG topics from ESRS Set 1 in simplified form.

The Comprehensive Module goes further, covering the specific datapoints that banks and investors need for their own regulatory obligations, including SFDR principal adverse impact (PAI) indicators, EBA Pillar 3 requirements, and the EU Benchmark Regulation.

For SMEs supplying to financial institutions or sustainability-focused investors, this alignment is what makes the Comprehensive Module worth the additional reporting effort.

Close

Key features of the VSME standard

One of the main goals of theVoluntary Sustainability Reporting Standard for non-listed SMEs (VSME) is to make ESG reporting as straightforward and accessible as possible. Unlike complex reporting frameworks designed for large corporations, the VSME introduces several key features that simplify the process for companies while still ensuring high-quality sustainability disclosures.

1. No materiality assessment required

In traditional ESG reporting frameworks, companies are often required to conduct a materiality assessment to determine which sustainability topics are relevant to their business. The CSRD for example requires that companies conduct a double materiality assessment. This process can be time-consuming and resource-intensive, especially for SMEs that often lack dedicated sustainability teams.

The VSME eliminates this burden by adopting an “if applicable” principle - meaning that companies only need to report on topics that are relevant to their business. If a specific disclosure does not apply to a company, there is no requirement to report on it.

2. Simplified language and reporting process

Many sustainability reporting standards use highly technical language and complex reporting structures, making it difficult for SMEs to comply. The VSME has been designed with:

Clear and simple terminology: Avoids jargon-heavy wording to make it easy to understand.

Predefined reporting templates: Standardised formats for disclosures help companies provide information in a structured and efficient way.

Checklists instead of lengthy narratives: Where possible, disclosures are structured as multiple-choice or quantitative data points rather than requiring detailed written explanations.

3. Modular approach to data collection

As we've already discussed the VSME's two-module system (Basic and Comprehensive) ensures that businesses can choose the level of detail they report based on their specific needs.

Basic Module: Provides a lightweight reporting framework with only 11 disclosures, focusing on essential ESG topics.

Comprehensive Module: Adds 9 additional disclosures for companies that need to report in greater detail.

This flexibility ensures that companies are not overwhelmed by unnecessary reporting requirements while still providing useful sustainability data to stakeholders.

4. No mandatory public disclosure

Unlike mandatory reporting frameworks, the VSME does not require businesses to publicly disclose their sustainability data. The primary purpose of the VSME is to facilitate ESG data sharing between companies and their business partners (such as banks, investors, and large companies).

SMEs can choose to:

Share their VSME report only with specific stakeholders (eg. lenders or suppliers).

Keep certain disclosures private if they contain sensitive business information.

Gradually expand their disclosures over time as they build ESG capabilities.

By reducing complexity, lowering costs, and protecting confidentiality, the VSME makes ESG reporting more accessible for SMEs and other companies, allowing them to participate in the sustainable economy without an excessive administrative burden.

The VSME’s design choices make it accessible, but they also involve trade-offs worth understanding.

What the VSME standard does not cover

The VSME is a genuinely useful tool for SME sustainability reporting, but understanding its limitations is just as important as understanding its benefits, particularly for companies trying to align with specific investor or lender expectations.

Scope 3 emissions are not required.

The Basic Module only covers Scope 1 and Scope 2 GHG emissions. Scope 3 — the indirect emissions across a company's value chain, which typically represent the largest share of a business's carbon footprint — is addressed in the EFRAG standard as information worth including where relevant, but it is not mandated by either module. For businesses working with clients or investors who expect full Scope 3 disclosure, the VSME alone may not be sufficient.

No third-party assurance is required.

Unlike CSRD reporting for large companies, the VSME does not require external audit or independent verification of the data reported. Companies can voluntarily seek limited assurance to strengthen stakeholder confidence, but there is no obligation to do so. This simplifies the process for SMEs, but means the credibility of a VSME report rests on the quality of the company's own data collection.

Voluntary uptake means inconsistent adoption.

The Commission Recommendation (EU) 2025/1710 encourages uptake but does not mandate it. Adoption rates vary across sectors and countries, meaning some SMEs may still encounter ad hoc ESG questionnaires from stakeholders who have additional data requirements beyond the VSME's scope.

Comparability across companies is limited.

As the Commission Recommendation makes clear, the VSME is designed to be proportionate, and companies can omit disclosures that are not applicable to their activities. The trade-off is that VSME reports are not always directly comparable across companies, a consideration worth keeping in mind for investors or analysts trying to benchmark SME sustainability performance.

VSME and GRI: how do they compare?

For companies already familiar with sustainability reporting, one of the most common questions about the VSME is how it relates to the GRI Standards — the most widely used voluntary reporting framework globally. The two are not in competition. They serve different purposes and different audiences, but they cover significant common ground.

The most important structural difference is in how topics are selected. GRI Standards require organisations to conduct a materiality assessment, a formal process of identifying the sustainability topics most significant to the business and its stakeholders. The VSME takes a different approach: disclosures are predefined, and the "if applicable" principle means a company simply omits any topic that does not apply to its circumstances. This makes VSME considerably lighter to implement, though it produces less granular and less customised reports than a full GRI disclosure.

The table below summarises the key differences:

Criteria

VSME

GRI Standards

Who it’s for

Non-listed SMEs (under 250 employees)

Organisations of all sizes, globally

Geographic scope

EU-specific

Global

Materiality assessment

Not required

Required (GRI 3: Material Topics)

Topic selection

Predefined disclosures

Determined by materiality assessment

Assurance

Not required

Not required (voluntary)

Legal status

Commission Recommendation

Voluntary framework

Scope 3 emissions

Not required

Encouraged where material

Despite these differences, the overlap in subject matter is substantial. VSME environmental disclosures correspond broadly to GRI 301–306 (materials, energy, water, biodiversity, emissions, waste), social disclosures to GRI 401–405 (employment, labour relations, occupational health, training, diversity), and governance metrics to GRI 205 (anti-corruption). Companies that have already built data infrastructure for GRI reporting will find they can reuse most of it for VSME without starting from scratch.

The reverse is also worth noting for SMEs thinking ahead: a company that starts with VSME and later needs to produce a GRI report will find that most of its quantitative data carries across, the main additions being the materiality assessment process and the greater narrative depth GRI expects.

How the VSME standard benefits companies

For many companies, sustainability reporting has been a costly and time-consuming challenge, with multiple stakeholders requesting ESG data in different formats. The Voluntary Sustainability Reporting Standard for SMEs (VSME) aims to simplify this process while offering strategic advantages for businesses that adopt it.

1. Reducing ESG reporting burden

Many companies face overlapping and uncoordinated ESG data requests from banks, investors, and corporate clients. The VSME provides a single, standardised framework, helping businesses:

🧾

Avoid the inefficiency of responding to multiple ESG questionnaires.

⏳

Reduce administrative costs and time spent on sustainability reporting.

📊

Provide a structured ESG report that meets most stakeholder expectations.

2. Improving access to financing

Businesses that can demonstrate sustainability commitments are more attractive to banks, investors, and funding programs. The VSME can help businesses:

📄

Strengthen loan applications by providing structured ESG data.

💼

Attract sustainability-focused investors.

🌱

Access green finance opportunities more easily.

3. Strengthening business relationships

Many large companies now require sustainability data from suppliers as part of their own ESG reporting. By adopting the VSME, companies can:

🔗

Meet supply chain sustainability requirements.

⚠️

Reduce the risk of losing contracts due to lack of ESG data.

🤝

Build trust with corporate clients and business partners.

4. Preparing for future regulations

Although the VSME is voluntary, ESG reporting requirements for businesses are evolving fast, and companies that start now will be better prepared to adapt.

Latest update: Omnibus I Directive in force since March 2026 The Omnibus I Directive (EU) 2026/470 was published in the Official Journal of the EU on 26 February 2026 and entered into force on 18 March 2026. It significantly narrowed the scope of mandatory CSRD reporting, raising the threshold to companies with more than 1,000 employees and over €450 million in net turnover. For SMEs, it also introduced a legally binding value chain cap: CSRD-reporting companies can no longer require suppliers with fewer than 1,000 employees to provide sustainability data beyond what the VSME standard specifies.

European Commission

Commission Recommendation (EU) 2025/1710, 30 July 2025

“The primary aim of this voluntary standard is to help undertakings not in scope of [the CSRD] to respond to information requests that they receive from financial institutions, large undertakings and other stakeholders.”

Importantly, the VSME remains a voluntary tool, but one that is increasingly seen as a stepping stone to future compliance. EU policymakers have reaffirmed that the VSME plays a complementary role in the EU’s sustainability reporting landscape. For SMEs, it offers a way to start building ESG capabilities now, in a proportionate and cost-effective manner, without waiting for legal obligations to catch up.

Adopting the VSME allows companies to:

🎯

Stay aligned with stakeholder expectations despite regulatory delays.

📊

Anticipate future reporting frameworks and reduce long-term compliance costs.

🏅

Position themselves competitively as sustainability becomes central to business decision-making.

5. Enhancing market positioning

Sustainability is becoming a key differentiator in many industries. Companies that report ESG data through the VSME can:

💡

Demonstrate ESG performance in a format stakeholders can assess and compare.

🌍

Build credibility with corporate clients who need ESG data for their own CSRD obligations.

🚀

Respond to client and investor ESG requests with a single standardised report.

What the Omnibus I Directive means for SMEs and VSME reporting

For SMEs supplying to large companies across the EU, the Omnibus I Directive (EU) 2026/470 is one of the most consequential regulatory developments in recent years. Adopted on 24 February 2026 and entering into force on 18 March 2026, it fundamentally reshaped the landscape of mandatory CSRD reporting in Europe, and it has direct consequences for how SMEs handle sustainability data requests.

The directive raised the threshold for mandatory CSRD reporting to companies with more than 1,000 employees and over €450 million in net turnover, removing an estimated 80% of companies previously in scope. While this relieves many mid-sized businesses of mandatory reporting obligations, it doesn’t mean ESG data requests from larger clients will stop. Companies that remain subject to the CSRD still need supply chain sustainability data to meet their own reporting requirements.

This is where the value chain cap becomes directly relevant to SMEs. The Omnibus I Directive introduced a legally binding rule: CSRD-reporting companies can no longer require suppliers or other value chain partners with fewer than 1,000 employees to provide sustainability data beyond what the VSME standard specifies. These smaller businesses are formally designated as "protected undertakings" under the directive, and any contractual clause that attempts to impose stricter requirements may be void. In practice, SMEs now have legal grounds to push back against excessive or uncoordinated ESG questionnaires from larger clients — and the VSME standard defines exactly what they can legitimately be asked to provide.

To understand the broader regulatory context and what the Omnibus I Directive means for your reporting obligations, read our guide to the EU Omnibus Regulation.

Next steps: How to get started

For businesses looking to adopt the Voluntary Sustainability Reporting Standard for SMEs (VSME), the process is designed to be flexible and scalable. While the standard is voluntary, using it effectively can help businesses meet stakeholder expectations, improve access to financing, and prepare for future sustainability requirements.

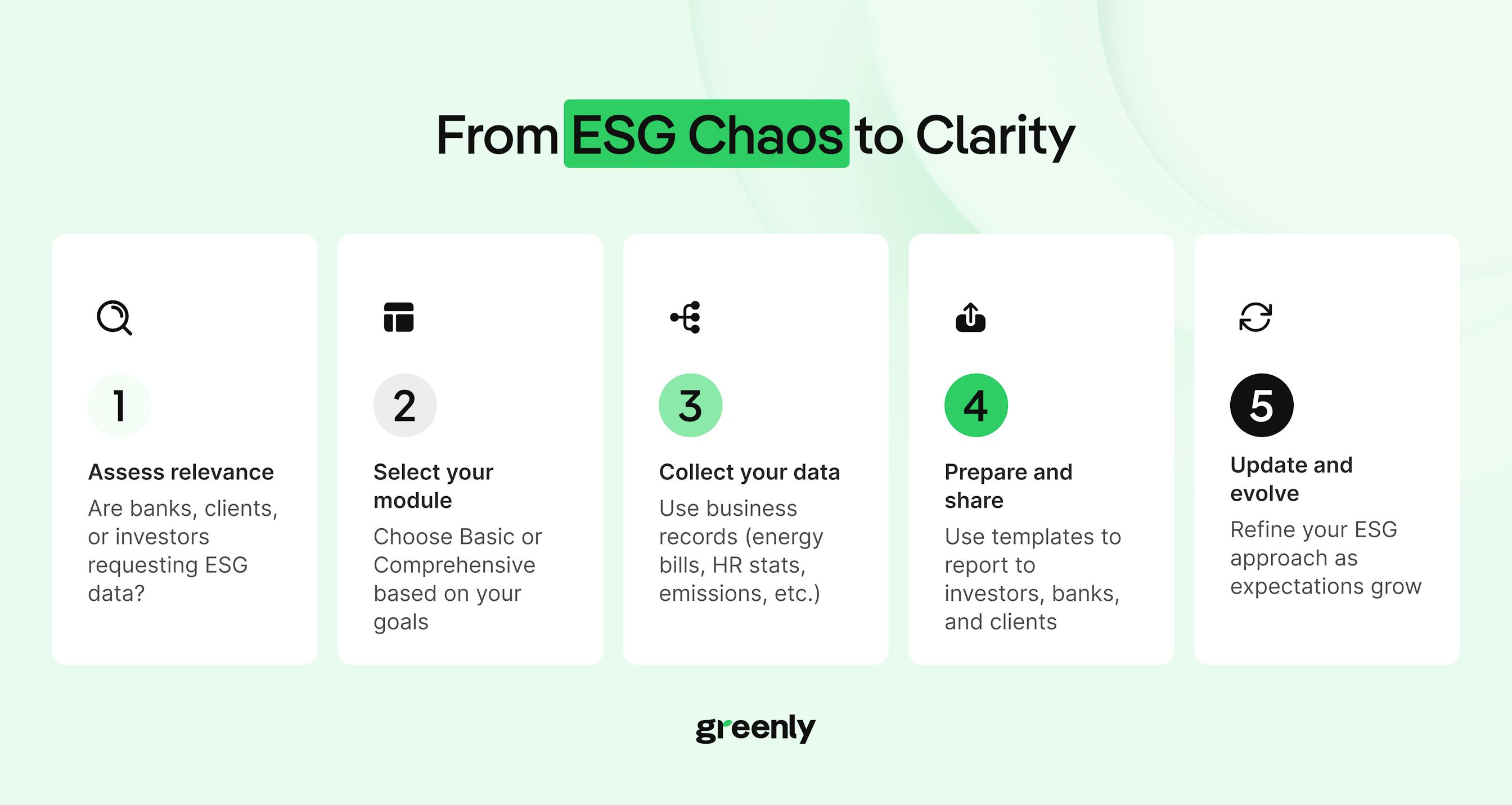

1. Determine whether the VSME is relevant to your business

Before adopting the VSME, companies should assess:

Are stakeholders (banks, investors, clients) asking for ESG data?

Does the business already track sustainability metrics?

Would a standardised framework reduce reporting burdens?

If ESG data requests are becoming more frequent, using the VSME can help provide a structured, widely recognised format that may replace multiple ad-hoc requests.

2. Choose the right reporting level

The VSME allows businesses to start small and expand reporting over time. The Basic Module covers core ESG disclosures and is suitable for companies looking to meet standard stakeholder expectations. The Comprehensive Module adds further disclosures for businesses that need to provide more in-depth ESG data, such as those seeking green financing or positioning themselves as sustainability leaders.

3. Gather the necessary ESG data

Once the module is selected, SMEs should review the required disclosures and begin collecting relevant data.

For SMEs new to ESG reporting, starting with existing business records (eg. energy bills, HR data) can simplify the process.

4. Prepare and share the report

The VSME is designed for internal use and communication with stakeholders rather than mandatory public disclosure. SMEs should:

Use predefined templates (if available) to structure disclosures.

Share reports with lenders, investors, and corporate partners as needed.

Regularly update ESG data to track progress and maintain transparency.

5. Stay informed on ESG trends and expectations

With the growing demand for ESG transparency, the VSME is expected to be widely adopted by financial institutions, investors, and corporate clients. To make the most of the standard, SMEs should:

Ensure they meet stakeholder expectations by keeping up to date with evolving ESG priorities.

Refine their reporting approach over time, using industry benchmarks to strengthen disclosures.

Explore sustainability initiatives or certifications that align with the VSME framework to enhance their credibility.

Close

For companies looking to put the VSME standard into practice, dedicated tools and expertise can make the process significantly more manageable.

How Greenly supports VSME reporting

For businesses adopting the Voluntary Sustainability Reporting Standard for SMEs (VSME), Greenly provides a comprehensive suite of tools, training, and expert guidance to simplify ESG data collection and strategy development. The VSME is designed for non-listed companies with fewer than 250 employees, though following the Omnibus I Directive, companies with up to 1,000 employees that fall outside the mandatory CSRD scope can also benefit from VSME-based reporting. This helps them build a solid foundation for future ESG reporting. To find out more about Greenly's VSME offer, visit our dedicated page.

1. ESG Data Collection & KPI Identification

Greenly streamlines the data collection process, helping businesses focus on the core sustainability metrics required under the VSME. Businesses can:

Identify key ESG data points relevant to investor and customer expectations.

Use personalised dashboards to track ESG performance and highlight key areas for improvement.

Increase their knowledge of ESG data, ensuring a strong foundation for future reporting requirements.

2. Training and Stakeholder Engagement

Building ESG expertise is crucial for long-term success. Greenly provides:

Comprehensive ESG training programmes to help teams understand sustainability metrics and reporting processes.

Workshops and webinars to educate businesses on ESG best practices.

Stakeholder identification - helping businesses to map out key investors, financial institutions, and corporate clients requesting ESG disclosures.

Guidance on selecting KPIs, ensuring that companies focus on meaningful sustainability indicators.

3. Business Intelligence for ESG Strategy

Greenly helps companies turn ESG data into a strategic asset, ensuring that VSME implementation strengthens long-term sustainability planning. This includes:

Identification of data gaps to ensure compliance completeness.

ESG Data Strategy Roadmap, prioritising actions to close data gaps efficiently.

4. Sustainability Reporting & Investor Communication

While VSME reporting is voluntary, Greenly makes it easy for businesses to share their ESG progress with key stakeholders:

Custom sustainability reports that can be shared with investors, clients, and financial institutions.

Data centralisation, ensuring ESG information is organised and accessible for future regulatory needs.

No data loss - everything reported under the VSME can be repurposed for future ESG reporting frameworks, such as the CSRD, ensuring compliance readiness.

By leveraging Greenly’s platform, businesses can save time, enhance ESG credibility, and build a strong foundation for their long-term sustainability strategy. Get in touch with us today to find out more.

Is the VSME standard mandatory?

No. The VSME is entirely voluntary. It was formally adopted as Commission Recommendation (EU) 2025/1710 on 30 July 2025, which encourages — but does not require — non-listed SMEs to use it. UK-based SMEs have no legal obligation to report under the VSME, though they may face practical pressure from EU clients, banks, or investors who use it as their standard data request format.

What is the difference between the VSME and the CSRD?

The CSRD is a mandatory EU directive applying to large companies and listed SMEs. It requires detailed reporting under the European Sustainability Reporting Standards (ESRS). The VSME is a voluntary, simplified framework for non-listed SMEs. It covers similar ESG topics to ESRS but with fewer disclosures, no double materiality assessment, and no assurance requirement.

Does the VSME require Scope 3 emissions reporting?

No. The Basic Module only requires Scope 1 and Scope 2 GHG emissions. The EFRAG standard notes that including Scope 3 data supports more complete reporting where relevant to the company’s sector, but it is not mandated by either module.

Can UK companies use the VSME?

Yes. The VSME is a voluntary framework, any company globally can choose to adopt it. For UK SMEs supplying to EU-based large companies subject to the CSRD, adopting the VSME is increasingly practical, as EU clients are expected to base their supplier ESG data requests on the VSME standard under the Omnibus I value chain cap.

What is the VSME Basic Module?

The Basic Module is the entry-level reporting tier, covering 11 disclosures across general information, environmental (energy, GHG emissions, water, biodiversity, pollution, circular economy), social (workforce, health and safety, remuneration), and governance (anti-corruption) topics. It is the minimum level of VSME adoption and is the required starting point before any company can apply the Comprehensive Module.

Does the VSME require a materiality assessment?

No. Unlike the CSRD, which requires a double materiality assessment, the VSME uses an "if applicable" principle. Companies only report on disclosures that are relevant to their circumstances. If a topic does not apply, it can simply be omitted, no explanation is required.

What does the Omnibus I value chain cap mean for SMEs?

Under the Omnibus I Directive (EU) 2026/470, which entered into force on 18 March 2026, CSRD-reporting companies can no longer require suppliers with fewer than 1,000 employees to provide sustainability data beyond what the VSME standard specifies. SMEs formally designated as "protected undertakings" under the directive can refuse requests that exceed the VSME’s scope.

Is the VSME the same as GRI?

No. The GRI Standards are a globally recognised framework that requires a materiality assessment, while the VSME is EU-specific, voluntary, and requires no materiality assessment. That said, the overlap in subject matter is substantial — VSME environmental disclosures broadly correspond to GRI 301–306 and social disclosures to GRI 401–405 — meaning companies already reporting under GRI can reuse much of their data for VSME without starting from scratch.

What about Greenly?

The VSME standard is no longer just a voluntary framework, it's quickly becoming the benchmark large companies are required to use when requesting ESG data from their suppliers. Understanding it, and reporting against it well, puts your business in a stronger position with every client, bank, and investor that asks.

Speak to Greenly about building a VSME report that works for your business today and scales with future requirements.