Decarbonisation: what it is and why it matters

1 min

Level

What is decarbonisation and why is it urgent? Learn practical steps companies can take to support the global move toward net zero emissions.

ESG / CSR

Industries

By Kara Anderson, UK Copywriter, on 04/03/2026

For a long time, sharing your company’s carbon footprint was a choice - usually a marketing one. But in 2026, that choice is disappearing. With the EU and California already moving toward mandatory disclosures, New York is now formalising its own requirements through Senate Bill S9072A.

Known as the Climate Corporate Data Accountability Act, this bill cleared the State Senate in February. It sends a clear message to large companies doing business in New York: the state is no longer asking for climate data; it is mandating it.

If your annual revenue exceeds $1 billion, you are on the hook. This isn't just about the electricity in your own offices; it includes your entire supply chain. Essentially, if you want to operate in the financial capital of the world, your emissions data is about to become as scrutinised as your financial statements.

The bill’s key requirements

Who Is Impacted

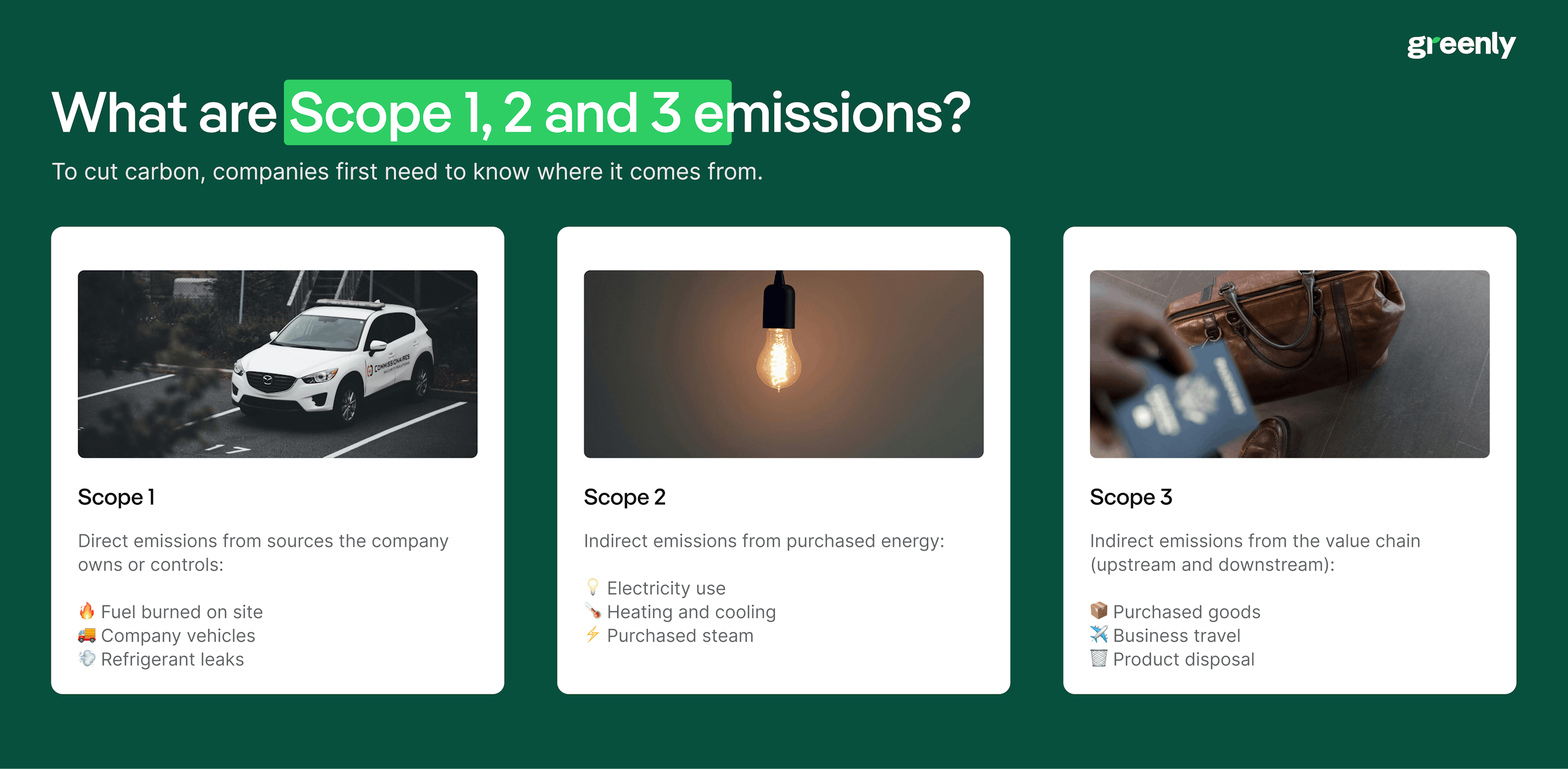

Reporting Scopes 1, 2, and 3

Timeline and deadlines

Enforcement and penalties

Senate Bill S9072A is New York’s move to bring corporate carbon footprints into the public eye. After passing the State Senate in February 2026, the bill is now under review by the Assembly. If signed into law, it will turn voluntary sustainability reports into a mandatory annual requirement for large companies.

The goal is simple: transparency. By providing investors, regulators, and the public with standardised data, New York aims to cut through the noise of greenwashing and provide a clear look at how the biggest players in the state are impacting the climate.

Under this proposal, companies won't be able to cherry-pick what they disclose. Instead, they must follow the GHG Protocol - the global gold standard for emissions accounting - to report across three specific categories: Scope 1, Scope 2, and Scope 3 emissions.

By requiring every major company to use the same "ruler", the bill makes it easy to compare one organisation to another. It effectively moves climate data from the marketing department to the compliance office, ensuring that disclosures are as standardised as financial statements.

S9072A isn't just for companies headquartered in New York - it’s designed to capture any large, U.S.-based corporation with a meaningful commercial presence here.

Under the current bill, you are considered a reporting entity if you meet two criteria:

The way the bill is drafted creates some important practical implications for larger organisations:

The bill does include exceptions for edge cases. For instance, a foreign entity isn't automatically pulled in just because it holds a board meeting or keeps a bank account in New York. There has to be an actual commercial connection to the state.

Current Status: As of March 4, 2026, the bill has officially cleared the Senate and is currently sitting with the Assembly Codes Committee.

At its core, S9072A is about moving corporate climate data from marketing highlights to a standardised annual requirement. Instead of companies picking and choosing what to disclose, the bill mandates a full accounting based on the GHG Protocol - the global standard for carbon bookkeeping.

Under the current draft, your reporting will be broken down into three distinct categories:

If S9072A becomes law, you won’t be expected to have every single data point ready overnight. The bill uses a phased rollout to give companies time to build the necessary tracking and verification systems.

Here is how the calendar looks:

This isn't just about a deadline - it’s about the complexity of the data. For most companies, measuring direct emissions (Scopes 1 and 2) is relatively straightforward. However, mapping out every supplier and customer use-case for Scope 3 takes significant time. The phased approach is a 'ready, set, go' model - giving you the 2026–2027 window to find the gaps in your data before the legal penalties start to apply.

S9072A isn't just a paperwork exercise. The bill is designed to move climate data into the same high-stakes category as financial reporting, and the enforcement mechanisms reflect that.

While the $100,000 daily penalty gets the headlines, the bigger risk for most corporations is reputational. These reports will be hosted on a public digital platform. In a market where investors, lenders, and customers are using this data to decide where to put their money, an "Inaccurate" or "Non-Compliant" tag from the Attorney General is a major red flag that can impact a company’s valuation and brand.

Even if S9072A is still moving through the Assembly, the direction of travel is clear: climate reporting is shifting to a hard regulatory requirement. If your company hits that $1 billion mark, here is how to start preparing.

The days of treating climate reporting as a voluntary exercise are over. States like New York and California are effectively setting the national standard, ensuring that transparency and accountability are built into the cost of doing business at scale. For organisations operating in New York, the message is simple: the more you do to formalise your emissions tracking now, the less risk you'll face when the first deadlines arrive in 2028.

Yes. Unlike many federal rules that only target public companies, S9072A applies to any U.S.-based entity - public or private - that does business in New York and meets the $1 billion revenue threshold.

The bill is designed to minimise duplication. If you are already preparing reports for California’s SB 253 or the EU’s CSRD, New York intends to let you submit those same reports, provided they meet the state’s specific criteria.

Yes. Reporting entities will be required to pay an annual fee to the Department of Environmental Conservation (DEC). These funds go into a new Climate Accountability and Emissions Disclosure Fund to pay for the program’s administration and digital public platform.

There is a "safe harbor" for Scope 3 emissions. Because supply chain data is famously difficult to track, the bill generally protects companies from penalties for Scope 3 errors made in good faith, at least during the initial rollout years.

The DEC is required to finalise the official regulations by December 31, 2027. However, because the first reporting wave in 2028 will cover your 2027 data, you effectively need your tracking systems ready by the start of next year.

If you are a UK-based firm, it depends on your U.S. structure. If your U.S. subsidiary does business in New York and the parent group hits the $1 billion revenue mark, you are likely in scope. The good news is that New York plans to accept reports already prepared for other jurisdictions, like the UK’s SDR or the EU’s CSRD. If you are already doing the work for UK regulators, you shouldn’t have to start from scratch for New York

Share this article

What is decarbonisation and why is it urgent? Learn practical steps companies can take to support the global move toward net zero emissions.

In this article, we’ll break down what IROs are, how to identify and assess them, and what CSRD requires in terms of disclosure.

In this article, we break down what the EU CBAM is, how it works, and what businesses need to do to comply.