CSRD Reporting:

Simplified for Success.

Take control of your compliance with a platform that turns reporting into

a foundation for long-term sustainability. Greenly makes managing your

CSRD obligations seamless.

TRUSTED BY 3,500 CLIENTS, FROM SMB TO ENTERPRISE

Integrated EFRAG-Compliant Scoring

Automated industry-specific materiality assessments to ensure your reporting remains fully aligned with EFRAG standards.

AI-Powered ESRS Data Collection

Streamline data mapping with AI-guided questions and tools to collect ESRS information effortlessly.

Automated xHTML & XBRL Reporting

Generate audit-ready reports in xHTML format, complete with integrated XBRL tagging for direct, seamless regulatory submission.

Expert Guidance at Every Stage

Partner with Greenly’s CSRD and Climate Experts through dedicated training, regular check-ins, and specialized tools to accelerate your progress.

The Only End-to-End CSRD Solution

With CSRD on the horizon, now’s the time to prepare and avoid wasting hours on compliance. Greenly’s platform offers expert guidance and tailored tools to ensure total regulatory readiness.

Greenly ensure a dedicated support at every step from experts trained directly by AFNOR and APAVE for CSRD auditing

Quickly check your company’s

CSRD requirements

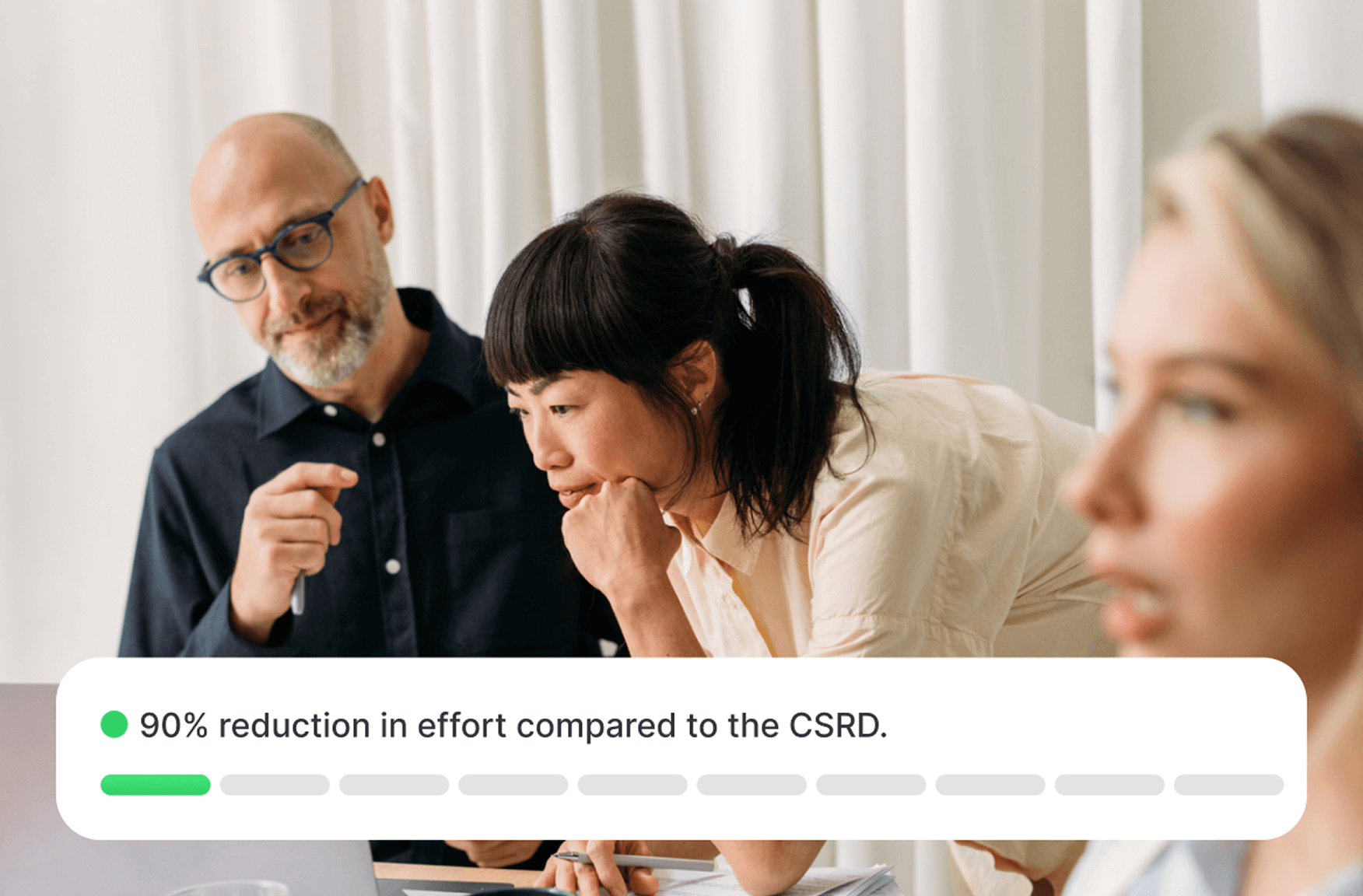

Cut CSRD Reporting Time From 1,000 Hours to Under 100

With CSRD on the horizon, now’s the time to prepare and avoid wasting hours on compliance. Greenly’s platform provides the expert guidance and specialized tools necessary to ensure total regulatory readiness.

An EFRAG-Aligned Foundation for Total Compliance

- Rigorous Double Materiality Methodology engineered by in-house experts specifically for CSRD audit standards

- Automated gap analysis to define and map the entire ESG data journey

- Actionable insights following gap analysis to ensure full regulatory compliance.

- CSRD-trained experts available to provide guidance and support at every step of the process

- ISSA 5000-aligned third-party auditor access to the Gap Analysis tool

- Integrated AI Assistant for real-time ESG guidance and support.

Comprehensive Coverage of 320+ ESRS Data Points

- Fully-integrated GHG platform for precise Scope 1, 2 and 3 assessments and Decarbonization Transition Plan

- Automatic calculation of quantitative data points through end-to-end modules (i.e. Waste, HR, etc)

- AI-powered narrative assistance that generates reporting insights directly from uploaded ESG data and API connections

- Sustainability performance monitoring and tracking in a single platform

- AI-powered internal audits, verified by sustainability experts to prevent errors and irregularities

Generate Fully Automated, Audit-Ready Reports

- Flawless formatting with integrated XBRL tagging and export-ready xHTML files

- Seamlessly align your data with global ESG standards, including CDP, ISSB, SEC, and SFRD

- Directly integrate EU Taxonomy exports into the final Sustainability Report

- Automatically generate and export Verification Reports finalized by third-party auditors

- Grant ISSA 5000-aligned access to third-party auditors while monitoring auditing progress in real-time

Streamlined Collaboration Across Functions and Entities

- Coordinated workflows to manage tasks, deadlines, and teams across multiple entities via an automated notification system

- Scalable multi-entity architecture built for organizations of any size, featuring granular access control

- Digital audit trails with time-stamped records for transparent accountability

- Integrated CRM system to eliminate manual follow-up and maintain accountability through automatic notifications

- Access to third-party auditors to give recommendations and feedback on data requirements & data quality level

- On-demand AI assistance to streamline workflows and optimize data processing

Future-Proof Your Business,

Master CSRD Compliance Today.

Deadlines are now. Become compliant to avoid fines.

What is the CSRD Directive?

The CSRD, or "Corporate Sustainability Reporting Directive," is a groundbreaking European directive that mandates certain companies to provide annual non-financial reporting.

Its primary goal is to enhance transparency by disclosing comprehensive and reliable information on companies' environmental and social impacts.

- Double Materiality Assessment and Due Diligence

- EU taxonomy system including XBRL tagging

- Governance-related information (management of sustainability risks)

- Mandatory third-party auditing

- Digitalization of sustainability reports in the The European Single Electronic Format (ESEF)

Does it apply to my company?

Following the 2026 Omnibus simplification package, the CSRD focuses on the largest EU market players, impacting approximately 15,000 companies, including the following:

Companies previously subject to the NFRD

- At least 500 employees

- More than 40 million euros turnover

- More than 25 million euros in the balance sheet

Report by 2025

Based on 2024

Report by 2025

Based on 2024

Large Enterprises

(Both listed and unlisted)

- At least 1,000 employees

- And either: 450 million euros turnover or 25 million euros in the balance sheet

Report by 2026

Based on 2025

Report by 2028

Based on 2027

Small and Medium sized Companies

(European and non-European)

- Listed SMEs are exempt and no longer required to report.

- Protected Status: Companies under 1,000 employees only need to use the Voluntary SME Standard (VSME) if asked for data by large partners.

Report by 2027

Based on 2026

Non-EU Parent Companies

- Over 450 million euros of EU turnover annually for 2 consecutive years

- Must have an EU subsidiary with 1,000+ employees or an EU branch with €200 million+ turnover

Report by 2029

Based on 2028

Report by 2029

Based on 2028

What are the data requirements?

European Sustainability Reporting Standards (ESRS) are the essential guidelines for CSRD reporting requirements. These include cross-cutting standards, such as ESRS 1 and ESRS 2, as well as topic-specific standards.

ESRS 1

ESRS 1 establishes the general principles to follow when preparing sustainability reporting.

- Double materiality assessment

- Sustainability due diligence

- Supply and value chain

- Timeline

ESRS 2

ESRS 2 consists of general disclosures and defines the mandatory baseline requirements, regardless of materiality assessment outcomes. The structure for topical standards is also established here:

- Governance: Disclosure Requirements 1-5

- Strategy: SBM 1-3

- Impacts, risks and opportunities - IRO 1-2 (based on Double Materiality Assessment)

- Metrics and targets

Environnement

Social

Governance

Not Impacted by CSRD? The VSME Standard is the Solution

Your company may not be impacted by the CSRD, but your largest clients are. Since 2025, they have been required to collect sustainability data from their entire value chain, including you.

The VSME standard, a must-have

- 90% less effort than the full CSRD

- Standardized format recognized by all large companies

- No mandatory audit (unlike the CSRD)

- Competitive advantage: be ready before your competitors

Why act now?

Leaders are preparing while their competitors wait. Within the next 12-18 months, your clients will demand this data. Those unable to provide it risk being replaced within the value chain.

With Greenly

- Simplified and guided questionnaire

- VSME report generated in one click

- Comprehensive training and support

- Trusted by over 3,500 companies

Still have questions?

Check out our complete FAQs in the Knowledge Base to get the answer you’re looking for.

The CSRD is an EU directive that strengthens sustainability reporting requirements on companies’ environmental, social, and governance (ESG) impacts.

Implementation is phased from 2024 to 2029. Notably, organizations with 500 –1,000 employees are eligible for a two-year transition exemption to facilitate the alignment process.

The CSRD now targets the largest firms (1,000+ employees). Listed SMEs are exempt, and non-listed SMEs are protected by voluntary reporting caps., check our article about it.

SMEs must prepare to disclose ESG data, monitor their carbon footprint, and assess supplier responsibility.

The CSRD is based on 12 ESRS (European Sustainability Reporting Standards) defined by EFRAG.

Tools like Greenly's help collect and structure ESG data, track carbon emissions, and meet CSRD standards easily. Book a demo with our Climate Experts to learn more.

Double materiality means reporting both how sustainability issues affect your business and how your business impacts people and the planet.

The CSRD and EU Taxonomy work together: companies must disclose how their activities align with the taxonomy’s environmental criteria in their ESG reports.

Penalties vary by country but can include fines, reputational damage, or exclusion from public and private tenders due to lack of ESG transparency.